Big Four accounting firms

The Big Four (Ernst & Young (EY), Deloitte & Touche, KPMG and PricewaterhouseCoopers (PwC) ) are the four biggest professional services networks in the world, offering audit, assurance services, taxation, management consulting, advisory, actuarial, corporate finance and legal services. They handle the vast majority of audits for public companies as well as many private companies.

Until the late 20th century, the market was dominated by eight networks but this gradually reduced due to mergers and the 2002 collapse of one firm, leaving four networks dominating the market in the early 21st century.

In the UK in 2011, it was reported that the Big Four audit 99% of the companies in the FTSE 100, and 96% of the companies in the FTSE 250 Index, an index of the leading mid-cap listing companies.[1] Such industry concentration has caused concern and calls for the Competition and Markets Authority to consider breaking up the Big Four. In October 2018, the CMA announced it had launched a detailed study of the Big Four's dominance of the audit sector.

List

| Firm | Revenues | Employees | Revenue per employee | Fiscal year | Headquarters | Source |

|---|---|---|---|---|---|---|

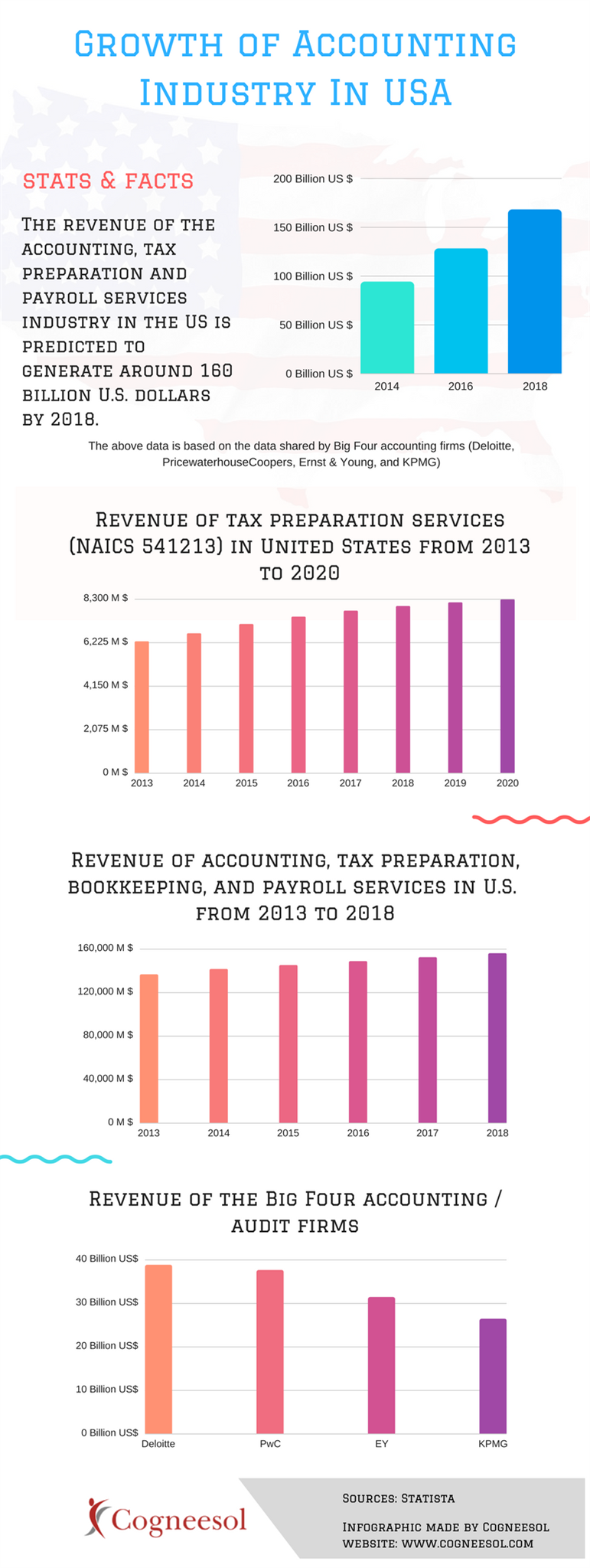

| Deloitte | $43.2 bn | 286,200 | $150,943 | 2018 | United Kingdom | [2] |

| PwC | $41.3 bn | 250,930 | $164,588 | 2018 | United Kingdom | [3] |

| EY | $34.8 bn | 260,000 | $133,846 | 2018 | United Kingdom | [4] |

| KPMG | $26.4 bn | 197,263 | $133,830 | 2017 | Netherlands | [5] |

This group was once known as the "Big Eight", and was reduced to the "Big Six" and then "Big Five" by a series of mergers. The Big Five became the Big Four after the fall of Arthur Andersen in 2002, following its involvement in the Enron scandal.

Legal structure

None of the Big Four firms is a single firm; rather, they are professional services networks. Each is a network of firms, owned and managed independently, which have entered into agreements with other member firms in the network to share a common name, brand and quality standards. Each network has established an entity to co-ordinate the activities of the network. In one case (KPMG), the co-ordinating entity is Dutch, and in three cases (Deloitte Touche Tohmatsu, PricewaterhouseCoopers (PwC) and Ernst & Young (EY)) the co-ordinating entity is a UK limited company. Those entities do not themselves perform external professional services and do not own or control the member firms. They are similar to law firm networks found in the legal profession.

In many cases each member firm practices in a single country, and is structured to comply with the regulatory environment in that country. In 2007, KPMG announced a merger of four member firms (in the United Kingdom, Germany, Switzerland and Liechtenstein) to form a single firm.

Ernst & Young (EY) also includes separate legal entities which manage three of its four areas: the Americas, EMEIA (Europe, the Middle East, India and Africa), and Asia-Pacific. (Note: the Japan area does not have a separate area management entity.) These firms coordinate services performed by local firms within their respective areas but do not perform services or hold ownership in the local entities.[6]

Mergers and the big auditors

Since 1989, mergers and one major scandal involving Arthur Andersen have reduced the number of major professional-services firms from eight to four.

Big Eight

The firms were called the Big Eight for most of the 20th century, reflecting the international dominance of the eight largest firms (presented here in alphabetical order):

- Arthur Andersen (until its closure in 2002 for a conviction related to the Enron scandal which was later overturned by the US Supreme Court)[7]

- Arthur Young

- Coopers and Lybrand (until 1973 Cooper Brothers in the UK and Lybrand, Ross Bros., & Montgomery in the United States)[8]

- Ernst & Whinney (until 1979 Ernst & Ernst in the United States and Whinney Murray in the UK)

- Deloitte Haskins & Sells (until 1978 Haskins & Sells in the United States and Deloitte & Co. in the UK)

- Peat Marwick Mitchell (later Peat Marwick, then KPMG)

- Price Waterhouse

- Touche Ross

Most of the Big Eight originated in an alliance formed between British and U.S. audit firms in the 19th or early 20th centuries. Price Waterhouse was a UK firm which opened a U.S. office in 1890 and subsequently established a separate U.S. partnership. The UK and U.S. Peat Marwick Mitchell firms adopted a common name in 1925. Other firms used separate names for domestic business, and did not adopt common names until much later: Touche Ross in 1960, Arthur Young (at first Arthur Young, McLelland Moores) in 1968, Coopers & Lybrand in 1973, Deloitte Haskins & Sells in 1978 and Ernst & Whinney in 1979.[9]

The firms' initial international expansion was driven by the needs of British and U.S.-based multinationals for worldwide service. They expanded by forming local partnerships or by forming alliances with local firms.

Arthur Andersen had a different history. The firm originated in the United States, and expanded internationally by establishing its own offices in other markets, including the United Kingdom.

In the 1980s the Big 8, each now with global branding, adopted modern marketing and grew rapidly. They merged with many smaller firms. One of the largest of these mergers was in 1987, when Peat Marwick merged with the Klynveld Main Goerdeler (KMG) group to become KPMG Peat Marwick, later known simply as KPMG.

Big Six

Competition among these firms intensified and the Big 8 became the Big Six in 1989 when Ernst & Whinney merged with Arthur Young to form Ernst & Young (EY) in June, and Deloitte, Haskins & Sells merged with Touche Ross to form Deloitte & Touche in August.

Confusingly, in the United Kingdom the local firm of Deloitte, Haskins & Sells merged instead with Coopers & Lybrand. For some years after the merger, the merged firm was called Coopers & Lybrand Deloitte and the local firm of Touche Ross kept its original name. In the mid 1990s however, both UK firms changed their names to match those of their respective international organizations. On the other hand, in Australia the local firm of Touche Ross merged instead with KPMG.[10][11] It is for these reasons that the Deloitte & Touche international organization was known as DRT International (later DTT International), to avoid use of names which would have been ambiguous (as well as contested) in certain markets.

Big Five

The Big 6 became the Big Five in July 1998 when Price Waterhouse merged with Coopers & Lybrand to form PricewaterhouseCoopers.

The Big 5 Accounting Firms were:[12]

- Ernst & Young (EY)

- Deloitte & Touche

- Arthur Andersen

- KPMG

- PricewaterhouseCoopers (PwC)

Big Four

- Ernst & Young (EY)

- Deloitte & Touche

- KPMG

- PricewaterhouseCoopers (PwC)

The Enron collapse and ensuing investigation prompted scrutiny of their financial reporting, which was audited by Arthur Andersen. Arthur Andersen was eventually indicted for obstruction of justice for shredding documents related to the audit in the 2001 Enron scandal. The resulting conviction, though later overturned, still effectively meant the end for Arthur Andersen. Most of its country practices around the world have been sold to members of what is now the Big Four—notably Ernst & Young globally; Deloitte & Touche in the UK, Canada, Spain, and Brazil; and PricewaterhouseCoopers (now known as PwC) in China and Hong Kong.

In 2010 Deloitte with its 1.8% growth was able to beat PricewaterhouseCoopers with its 1.5% growth to gain first place and become the largest firm in the industry. In 2011, PwC re-gained the first place with 10% revenue growth. In 2013, these two firms still claim the top two spots with only $200 million or 0.5% revenue difference. However, Deloitte has seen faster growth than PwC over the last few years (largely due to acquisitions) and reclaimed the title of largest of the Big Four in Fiscal Year 2016.

{kind=link}

It was estimated that the Big Four had about 67 per cent share of the global accountancy market in 2012 while the rest were divided amongst so-called mid-tier players, including Grant Thornton and BDO.[13]

Branding list

A year at the end indicates year of formation through merger or adoption of single brand name.

- Arthur Andersen (1913–2002)

- Ernst & Young (EY) (1989) (Ernst & Young until 2013)

- Arthur Young (1906)

- Ernst & Whinney (EY) (1979)

- Ernst & Ernst (US) (1903)

- Whinney, Smith & Whinney (UK) (1849)

- PriceWaterhouseCoopers (PwC) (1998) (PricewaterhouseCoopers until 2010)

- Coopers & Lybrand (1973)

- Cooper Brothers (UK) (1854)

- Lybrand, Ross Bros, Montgomery (US) (1898)

- Price Waterhouse (US) (1849)

- Coopers & Lybrand (1973)

- Deloitte Touche Tohmatsu (1989) (Deloitte & Touche until 1993)

- Deloitte Haskins & Sells (1978)

- Deloitte & Co. (UK) (1845)

- Haskins & Sells (US) (1895)

- Touche Ross (1975)

- Touche Ross (1960) (Touche, Ross, Bailey & Smart until 1969)

- Ross (Canada)

- George A. Touche (UK)

- Touche, Niven, Bailey & Smart (US) (1947)

- Touche Niven (1900)

- Bailey & Smart (1947)

- Tohmatsu & Co. (Japan) (1968)

- Touche Ross (1960) (Touche, Ross, Bailey & Smart until 1969)

- Deloitte Haskins & Sells (1978)

- KPMG (1987) (KPMG Peat Marwick before 1995)

- Peat Marwick (1925) (originally Peat Marwick Mitchell)

- William Barclay Peat (UK) (1870)

- Marwick Mitchell (US) (1897)

- Edwin Gurthie (1875–1955)

- Beevers & Adgie (1849–1967)

- KMG (1979) (officially Klynveld Main Goerdeler)

- Klynveld Kraayenhof (Netherlands) (1917)

- McLintock Main Lafrentz (1964)

- Thomson McLintock (UK) (1877)

- Martin Farlow (1882–1968)

- Grace Ryland (1967–1969)

- Grace, Darbyshire, & Todd (1818)

- CJ Ryland (1910)

- Main Lafrentz (US) (c.1880)

- Thomson McLintock (UK) (1877)

- Deutsche Treuhand-Gesellschaft (Germany) (1890)

- Armitage & Norton (1869–1987)

- Peat Marwick (1925) (originally Peat Marwick Mitchell)

Criticism

Tax avoidance

According to Australian taxation expert George Rozvany, the Big Four are "the masterminds of multinational tax avoidance and the architects of tax schemes which cost governments and their taxpayers an estimated $US1 trillion a year". At the same time they are advising governments on tax reforms, they are advising their multinational clients how to avoid taxes.[14][15]

Policy issues concerning industry concentration

In the wake of industry concentration and individual firm failure, the issue of a credible alternative industry structure has been raised.[16] The limiting factor on the growth of additional firms is that although some of the firms in the next tier have become quite substantial, and have formed international networks, effectively all very large public companies insist on having a "Big Four" audit, so the smaller firms have no way to grow into the top end of the market.

Documents published in June 2010 show that some UK companies' banking covenants required them to use one of the Big Four. This approach from the lender prevents firms in the next tier from competing for audit work for such companies. The British Bankers' Association said that such clauses are rare.[17] Current discussions in the UK consider outlawing such clauses.

In 2011,The UK House of Lords completed an inquiry into the financial crisis, and called for an Office of Fair Trading investigation into the dominance of the Big Four.[18] It is reported that the Big Four audit all but one of the companies that constitute the FTSE 100, and 240 of the companies in the FTSE 250, an index of the leading mid-cap listing companies.[1]

In Ireland, the Director of Corporate Enforcement, in February 2011 said, auditors "report surprisingly few types of company law offences to us", with the so-called "big four" auditing firms reporting the least often to his office, at just 5pc of all reports.[19]

The January 2018 collapse of the UK construction and services company Carillion raised further questions about the Big Four, all of which had advised the company before its liquidation. On 13 February 2018, the Big Four were described by MP and chair of the Work and Pensions Select Committee Frank Field as "feasting on what was soon to become a carcass" after collecting fees of £72m for Carillion work during the years leading up to its collapse.[20] The final report of a Parliamentary inquiry into the collapse of Carillion, published on 16 May 2018,[21] accused the Big Four accounting firms of operating as a "cosy club", with KPMG singled out for its "complicity" in signing off Carillion’s "increasingly fantastical figures" and internal auditor Deloitte accused of failing to identify, or ignoring, "terminal failings". The report recommended the Government refer the statutory audit market to the Competition and Markets Authority, urging consideration of breaking up the Big Four.[21] In September 2018, Business Secretary Greg Clark announced he had asked the CMA to conduct an inquiry into competition in the audit sector,[22] and on 9 October 2018, the CMA announced it had launched a detailed study.[23]

Global member firms

| Region | Deloitte Touche Tohmatsu | PwC | Ernst & Young | KPMG |

|---|---|---|---|---|

| Australia | Deloitte Australia[24] | PricewaterhouseCoopers | Ernst & Young | KPMG |

| Argentina | Deloitte & Co. S.A[25]. | Pricewaterhouse & Co. S.R.L[26]. | Ernst & Young | KPMG |

| Bangladesh | Not Active | PwC[27] | A. Qasem & Co., Chartered Accountants | Rahman Rahman Huq & Co., Chartered Accountants |

| Brazil | Deloitte | PwC[28] | EY | KPMG |

| Bulgaria | Deloitte | PwC[29] | EY | KMPG |

| Cambodia | Deloitte | PricewaterhouseCoopers (Cambodia) Ltd.[30] | Ernst and Young | KMPG |

| Canada | Deloitte | PwC[31] | EY | KPMG |

| China | Deloitte Hua Yong | PricewaterhouseCoopers Zhong Tian[32] | Ernst & Young Hua Ming | KPMG Hua Zhen |

| Egypt | Saleh, Barsoum & Abdel Aziz | Mansour & Co.[33] | Allied for Accounting and Auditing (Emad Ragheb) | Hazem Hassan |

| El Salvador | DTT El Salvador, S.A. de C.V. | PricewaterhouseCoopers El Salvador[34] | Ernst & Young El Salvador, S.A. de C.V. | KPMG, S.A. |

| Finland | Deloitte & Touche Oy | PricewaterhouseCoopers Oy[35] | Ernst & Young Oy | KPMG Oy Ab |

| France | EY TRANSACTION SERVICES | KPMG | ||

| Ghana | Deloitte | PwC[36] | EY | KPMG |

| Hong Kong | Deloitte | PricewaterhouseCoopers[37] | Ernst & Young | KPMG |

| India | Deloitte | PricewaterhouseCoopers[38] | EY | KPMG |

| Indonesia | KAP Satrio Bing Eny & Rekan | KAP Tanudiredja, Wibisana, Rintis & Rekan[39] | KAP Purwantono, Sungkoro & Surja | KAP Sidharta Widjaja & Rekan |

| Israel | Deloitte Brightman Almagor Zohar | Kesselman & Kesselman, PwC Israel[40] | Kost, Forer, Gabbay & Kasierer (Ernst & Young Israel) | KPMG Somekh Chaikin |

| Italy | Deloitte Touche Tohmatsu | PricewaterhouseCoopers | Reconta Ernst & Young SpA, Ernst & Young Financial Business Advisors SpA, | KPMG S.p.A., KPMG Advisory S.p.A., KPMG Fides S.p.A. |

| Japan | Deloitte Touche Tohmatsu Kansa Houjin Tohmatsu |

PricewaterhouseCoopers Aarata Aarata Kansa Houjin PricewaterhouseCoopers Kyoto |

Ernst & Young ShinNihon LLC ShinNihon Yugen-sekinin Kansa Houjin |

KPMG AZSA LLC (formerly KPMG AZSA & Co.) Azsa Kansa Houjin |

| Jordan | Deloitte Touche (M.E) | PwC | Ernst & Young | KPMG |

| Kazakhstan | Deloitte | PwC | EY | KPMG |

| Kenya | Deloitte & Touche (E.A) | PwC | Ernst & Young | KPMG |

| Kyrgyzstan | Deloitte | - | EY | KPMG |

| Lebanon | Deloitte Touche (M.E) | PwC | Ernst & Young | KPMG PCC |

| Malaysia | Deloitte PLT | PricewaterhouseCoopers | Ernst & Young | KPMG |

| Malta | Deloitte | PwC | EY Malta | KPMG |

| Mexico | Galaz, Yamazaki, Ruiz Urquiza, S.C. | PricewaterhouseCoopers México | Mancera S.C. | KPMG Cárdenas Dosal, S.C. |

| Mongolia | Deloitte Onch | PwC | Ernst & Young Mongolia | KPMG |

| Morocco | Deloitte Touche (M.E) | PwC | Ernst & Young | KPMG |

| New Zealand | Deloitte | PwC | EY | KPMG |

| Nigeria | Akintola Williams Deloitte | PwC Nigeria | Ernst & Young | KPMG |

| Pakistan | Deloitte Yousuf Adil | A. F. Ferguson & Co. | EY Ford Rhodes | KPMG Taseer Hadi & Co. |

| Palestinian Territories | Deloitte Touche (M.E) | PwC | Ernst & Young | none |

| Peru | DELOITTE & TOUCHE SRL | PRICEWATERHOUSECOOPERS S.CIVIL DE R.L. | ERNST & YOUNG SRL | KPMG SAC |

| Philippines | Navarro Amper & Co (formerly Manabat Delgado Amper & Co.) | Isla Lipana & Co. | SyCip Gorres Velayo & Co. | R.G. Manabat & Co. (formerly Manabat Sanagustin & Co.) |

| Poland | Deloitte | PwC | EY | KPMG |

| Romania | Deloitte Audit S.R.L., Deloitte Tax S.R.L., Deloitte Consultanta S.R.L., Deloitte Evaluare S.R.L. Deloitte Fiscal Representative S.R.L. and Reff & Associates SCA (jointly referred to as "Deloitte Romania")[41] | PricewaterhouseCoopers Audit SRL, PricewaterhouseCoopers Tax Advisors & Accountants SRL, PricewaterhouseCoopers Management Consultants SRL, PricewaterhouseCoopers Business Recovery Services IPURL, PricewaterhouseCoopers Servicii SRL[42] | Ernst & Young Romania SRL[43] | KPMG Romania S.R.L.[44] |

| Saudi Arabia | Deloitte & Touche Bakr Abulkhair & Co | PricewaterhouseCoopers LLP | Ernst & Young Saudi Arabia | KPMG Al Fozan & Partners |

| Serbia | Deloitte d.o.o. Beograd[45] | PricewaterhouseCoopers d.o.o. Beograd[46] | Ernst & Young d.o.o. Beograd[47] | KPMG d.o.o Beograd[48] |

| Slovak Republic | Deloitte Audit s.r.o. | PricewaterhouseCoopers Slovensko, s.r.o. | Ernst & Young Slovakia, spol. s r.o. | KPMG Slovensko spol. s r.o. |

| South Africa | Deloitte | PwC | EY | KPMG |

| South Korea | Anjin LLC | Samil LLC | Hanyoung LLC | Samjong LLC |

| Sri Lanka | SJMS Associates (independent correspondent firm) | PwC | Ernst & Young | KPMG |

| Sweden | Deloitte Touche Tohmatsu | Öhrlings PricewaterhouseCoopers | Ernst & Young | KPMG |

| Syria | Deloitte (M.E) - Nassir Tamimi Chartered Accountant | PricewaterhouseCoopers | Abdul Kader Hussarieh and partners | Mejanni & Co. Chartered Accountants and Consultants LLC |

| Thailand | Deloitte & Touche Tohmatsu | PricewaterhouseCoopers | Ernst & Young | KPMG |

| Taiwan | Deloitte | PricewaterhouseCoopers Taiwan | Ernst & Young | KPMG |

| Turkey | DRT Bagimsiz Denetim ve S.M.M. A.S. | Basaran Nas Bagimsiz Denetim ve SMMM A.S. | Güney Bağımsız Denetim ve S.M.M. A.Ş., Kuzey Y.M.M. Denetim A.Ş., Ernst Young Kurumsal Finansman Danışmanlık A.Ş., BEY S.M.M. A.Ş. | Akis Bagimsiz Denetim ve S.M.M. A.S. |

| Uzbekistan | Deloitte Touche Tohmatsu | ASC PricewaterhouseCoopers | Ernst & Young LLC | KPMG Audit LLC |

| Venezuela | Lara Marambio & Asociados - Deloitte | Pacheco, Apostólico & Asociados - PricewaterhouseCoopers | EY | Rodriguez Velasquez & Asociados - KPMG |

| Uganda | Deloitte | PwC | EY | KPMG |

| Zimbabwe | Deloitte | PwC | EY | KPMG |

Big Four using AI tools

Currently, Big 4 accounting firms are trying to increase their use of AI tools. Some only acquire AI tools from a single vendor and the others acquire multiple functions from different vendors and integrate into their own systems. However, most of the AI tools used now do not have advanced capability and need human's operations. Besides Deloitte, EY worked on data science tools and PwC has a software called Halo to analyze journal entries. Some tasks have been replaced by machines, but most of the jobs need to be done by auditors. [49]

See also

References

- 1 2 Mario Christodoulou (2011-03-30). "U.K. Auditors Criticized on Bank Crisis". Wall Street Journal.

- ↑ "Deloitte announces record revenue of US$43.2 billion". Deloitte. 18 September 2018. Retrieved 7 October 2018.

- ↑ PricewaterhouseCoopers. "PwC revenues grow by 7% to record US$37.7 billion". PwC.

- ↑ http://www.ey.com/gl/en/newsroom/news-releases/news-ey-reports-record-global-revenues-in-2016-up-by-9-percent

- ↑ "2017 KPMG International Annual Review" (PDF). Retrieved 14 December 2017.

- ↑ "Legal Disclaimer". Ernst & Young. Retrieved 2016-10-11.

- ↑ ARTHUR ANDERSEN LLP, PETITIONER v. UNITED STATES 544 U.S. 696

- ↑ News, From Bloomberg (1997-09-19). "Coopers, Price Waterhouse Plan to Merge". Los Angeles Times. ISSN 0458-3035. Retrieved 2017-11-09.

- ↑ "What's in a name: Firms' simplified family trees on the web". icaew.com.

- ↑ http://www.deloitte.com/dtt/article/0,1002,cid%253D12279,00.html

- ↑ Alison Leigh Cowan (1989-12-05). "Deloitte, Touche Merger Done". New York Times.

- ↑ https://big4accountingfirms.com/big-5-accounting-firms/

- ↑ Fleming, Sam (12 Feb 2014). "Accountants PwC, Deloitte, KPMG and EY face taming moves". The Financial Times. Retrieved 6 May 2017.

- ↑ "'Tax avoidance' masters revealed". The NEWDAILY. 2016-07-11.

- ↑ "'Big Four' audit firms never examined over illegal tax plans". The Independent. 2016-01-18.

Regulators fail to act as they are dominated by the companies they are supposed to police, say critics

- ↑ "Too Big to Fail: Moral Hazard in Auditing and the Need to Restructure the Industry Before it Unravels". ssrn.com. SSRN 928482.

- ↑ "Big-Four-only clauses are rare: BBA". accountancyage.com. Archived from the original on 2010-06-21.

- ↑ "Auditors criticised for role in financial crisis". Financial Times.

- ↑ http://www.independent.ie/business/irish/appleby-and-revenue-query-work-of-auditors-2544309.htm

- ↑ Davies, Rob (13 February 2018). "Carillion: accountants accused of 'feasting' on company". Guardian. Retrieved 13 February 2018.

- 1 2 Davies, Rob (16 May 2018). "'Recklessness, hubris and greed' – Carillion slammed by MPs". Guardian. Retrieved 16 May 2018.

- ↑ Busby, Mattha (29 September 2018). "Audit sector faces inquiry as minister points to deficiencies". Guardian. Retrieved 29 September 2018.

- ↑ "CMA launches immediate review of audit sector". Gov.uk. Retrieved 9 October 2018.

- ↑ "About Deloitte Australia". Deloitte Australia. 20 February 2015. Retrieved 6 October 2015.

- ↑ "Deloitte Argentina".

- ↑ "PwC Argentina".

- ↑ "PwC Bangladesh".

- ↑ "Brazil Office Address".

- ↑ "Bulgaria PwC Offices Locations".

- ↑ "Cambodia PwC Offices Addresses".

- ↑ "Canada PwC Offices Addresses".

- ↑ "China PwC Offices Addresses".

- ↑ "Egypt PwC Offices Addresses".

- ↑ "El Salvador PwC Offices Addresses".

- ↑ "Finland PwC Offices Addresses".

- ↑ "Ghana PwC Offices Addresses".

- ↑ "Hong Kong PwC Offices Addresses".

- ↑ "India PwC Offices Addresses".

- ↑ "Indonesia PwC Offices Addresses".

- ↑ "Israel PwC Offices Addresses".

- ↑ "Archived copy". Archived from the original on 2014-08-08. Retrieved 2014-08-07.

- ↑ PricewaterhouseCoopers. "About site provider". PwC.

- ↑ "Members :: CCE-R". ccer.ro. Archived from the original on 2014-08-10.

- ↑ "Home - KPMG - RO". kpmg.com.

- ↑ "Serbia Business Registry Agency - Deloitte results".

- ↑ "Serbia Business Registry Agency - PwC results".

- ↑ "Serbia Business Registry Agency - EY results".

- ↑ "Serbia Business Registry Agency - KPMG results".

- ↑ Kokina, Julia; Davenport, Thomas H. (March 2017). "The Emergence of Artificial Intelligence: How Automation is Changing Auditing". Journal of Emerging Technologies in Accounting. 14 (1): 115–122. doi:10.2308/jeta-51730.

External links

- Official website Deloitte

- Official website Ernst & Young

- Official website PricewaterhouseCoopers

- Official website KPMG

- International Consortium of Investigative Journalists, Big 4 Audit Firms Play Big Role in Offshore Murk,

- G8 And Tax Avoidance - Spinwatch Exclusive on the role of the Big Four in lawmaking

- Blockchain consulting and development services

- International Tax Consulting Services