Directional-change intrinsic time

Directional-change intrinsic time is an event-based operator to dissect a data series into a sequence of alternating trends of defined size .

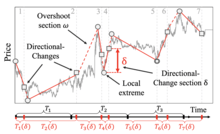

The directional-change intrinsic time operator was developed for the analysis of financial market data series. It is an alternative methodology to the concept of continuous time.[1] Directional-change intrinsic time operator dissects a data series into a set of drawups and drawdowns or up and down trends that alternate with each other. An established trend comes to an end as soon as a trend reversal is observed. A price move that extends a trend is called overshoot and leads to new price extremes.

Figure 1 provides an example of a price curve dissected by the directional change intrinsic time operator.

The frequency of directional-change intrinsic events maps (1) the volatility of price changes conditional to (2) the selected threshold . The stochastic nature of the underlying process is mirrored in the non-equal number of intrinsic events observed over equal periods of physical time.

Directional-change intrinsic time operator is a noise filtering technique. It identifies regime shifts, when trend changes of a particular size occur and hides price fluctuations that are smaller than the threshold .

References

- Guillaume, Dominique M.; Dacorogna, Michel M.; Davé, Rakhal R.; Müller, Ulrich A.; Olsen, Richard B.; Pictet, Olivier V. (1997-04-01). "From the bird's eye to the microscope: A survey of new stylized facts of the intra-daily foreign exchange markets". Finance and Stochastics. 1 (2): 95–129. doi:10.1007/s007800050018. ISSN 0949-2984.

- Glattfelder, J. B.; Dupuis, A.; Olsen, R. B. (2011-04-01). "Patterns in high-frequency FX data: discovery of 12 empirical scaling laws". Quantitative Finance. 11 (4): 599–614. arXiv:0809.1040. doi:10.1080/14697688.2010.481632. ISSN 1469-7688.

- Guillaume, Dominique M.; Dacorogna, Michel M.; Davé, Rakhal R.; Müller, Ulrich A.; Olsen, Richard B.; Pictet, Olivier V. (1997-04-01). "From the bird's eye to the microscope: A survey of new stylized facts of the intra-daily foreign exchange markets". Finance and Stochastics. 1 (2): 95–129. doi:10.1007/s007800050018. ISSN 0949-2984.

- Golub, Anton; Glattfelder, James; Olsen, Richard B. (2017-04-05). "The Alpha Engine: Designing an Automated Trading Algorithm". Rochester, NY. SSRN 2951348. Cite journal requires

|journal=(help) - Golub, Anton; Chliamovitch, Gregor; Dupuis, Alexandre; Chopard, Bastien (2016-01-01). "Multi-scale representation of high frequency market liquidity". Algorithmic Finance. 5 (1–2): 3–19. doi:10.3233/AF-160054. ISSN 2158-5571.