Concentration of media ownership

Concentration of media ownership (also known as media consolidation or media convergence) is a process whereby progressively fewer individuals or organizations control increasing shares of the mass media.[1] Contemporary research demonstrates increasing levels of consolidation, with many media industries already highly concentrated and dominated by a very small number of firms.[2][3]

| Journalism |

|---|

| Areas |

| Genres |

|

| Social impact |

| News media |

| Roles |

|

Globally, large media conglomerates include Bertelsmann, National Amusements (ViacomCBS), Sony Corporation, News Corp, Comcast, The Walt Disney Company, AT&T Inc., Fox Corporation, Hearst Communications, MGM Holdings Inc., Grupo Globo (South America) and Lagardère Group.[4][5][6]

As of 2020, the largest media conglomerates in terms of revenue rank Comcast, The Walt Disney Company, AT&T and ViacomCBS per Forbes.

In nations described as authoritarian by most international think-tanks and NGOs, media ownership is generally something very close to the complete state control over information in direct or indirect ways.

Mergers

Media mergers are a result of one media related company buying another company for control of their resources in order to increase revenues and viewership. As information and entertainment become a major part of our culture, media companies have been creating ways to become more efficient in reaching viewers and turning a profit. Successful media companies usually buy out other companies to make them more powerful, profitable, and able to reach a larger viewing audience. Media mergers have become more prevalent in recent years, which has people wondering about the negative effects that could be caused by media ownership becoming more concentrated. Such negative effects that could come into play are lack of competition and diversity as well as biased political views.[7]

Steven Rattner an expert in the field of media mergers and acquisitions who is a professional investment banker stated that "we are entering what may will prove to be the golden age of competition in communications industries." [8] The idea of media merger is a relatively new concept that we will continue to see affect the impact and spread of communication.

There have been 5 prominent media mergers that have truly restructured the world of media as we know it.

Fox Business states that these are the 5 biggest media mergers of all time:

The biggest media merger of all time is America Online which bought control over Time Warner Incorporated in the year of 2000 on January 10th for a total of 112 billion dollars.

The second biggest media merger of all time is AT&T buying control over Time Warner Incorporated once again this time in the year of 2016 on October 22nd for a total of 101 billion dollars.

The third biggest media merger of all time is Charter Communications buying control over Time Warner Incorporated for the 3rd time in the year of 2015 on May 26th for a total of 87.4 Billion dollars.

The fourth largest media merger of all time is Walt Disney Company buying control over Twenty First Century Fox Incorporated the sector of their entertainment business in the year of 2017 on December 14th for a total of 84.8 Billion dollars.

The fifth largest media merger of all time is AT&T buying control over direcTV in the year of 2014 on May 18th for a total of 66.5 Billion dollars.

Media oligopoly

An oligopoly is when a few firms dominate a market.[9] The term oligopoly comes from the phrase oligarchy. Merriam Webster- Dictionary defines oligarchy as "a government in which a small group exercises control especially for corrupt and selfish purposes" So, When the larger scale media companies buy out the more smaller-scaled or local companies they become more powerful within the market. As they continue to eliminate their business competition through buyouts or forcing them out (because they lack the resources or finances) the companies left dominate the media industry and create a media oligopoly.[7]

Risks for media integrity

Media integrity is at risk when small number of companies and individuals control the media market. Media integrity refers to the ability of a media outlet to serve the public interest and democratic process, making it resilient to institutional corruption within the media system, economy of influence, conflicting dependence and political clientelism.[10] Media integrity is especially endangered in the case when there are clientelist relations between the owners of the media and political centres of power. Such a situation enables excessive instrumentalisation of the media for particular political interests, which is subversive for the democratic role of the media.

Elimination of net neutrality

Net neutrality is also at stake when media mergers occur. Net neutrality involves a lack of restrictions on content on the internet, however, with big businesses supporting campaigns financially they tend to have influence over political issues, which can translate into their mediums. These big businesses that also have control over internet usage or the airwaves could possibly make the content available biased from their political stand point or they could restrict usage for conflicting political views, therefore eliminating net neutrality.[9]

While there was a large awareness and concern surrounding net neutrality rights in the late months in the year of 2017. This is still a prominent issue even though it does not still have the presence on social media. Net neutrality is already a fragile and sought after commodity than many regions do not have access to. "See, net neutrality keeps internet providers in check, if you will. Without net neutrality, there would be a sort of monopoly over the internet, and rather than having the freedom to roar just about any and every inch of the online world, companies could start to dictate where you are allowed to go."

Issues

Concentration of media ownership is very frequently seen as a problem of contemporary media and society.[4][5][6] When media ownership is concentrated in one or more of the ways mentioned above, a number of undesirable consequences follow, including the following:

- Commercially driven, ultra-powerful mass market media is primarily loyal to sponsors, i.e. advertisers and government rather than to the public interest.

- Only a few companies representing the interests of a minority elite control the public airwaves.

- Healthy, market-based competition is absent, leading to slower innovation and increased prices.

Diversity of viewpoints

It is important to elaborate upon the issue of media consolidation and its effect upon the diversity of information reaching a particular market. Critics of consolidation raise the issue of whether monopolistic or oligopolistic control of a local media market can be fully accountable and dependable in serving the public interest.

Freedom of the press and editorial independence

On the local end, reporters have often seen their stories refused or edited beyond recognition. An example would be the repeated refusal of networks to air "ads" from anti-war advocates to liberal groups like MoveOn.org, or religious groups like the United Church of Christ, regardless of factual basis. Journalists and their reports may be directly sponsored by parties who are the subject of their journalism leading to reports which actually favor the sponsor, have that appearance, or are simply a repetition of the sponsors' opinion.[11][12][13]

Consequently, if the companies dominating a media market choose to suppress stories that do not serve their interests, the public suffers, since they are not adequately informed of some crucial issues that may affect them.

Concern among academia rests in the notion that the purpose of the First Amendment to the US constitution was to encourage a free press as political agitator evidenced by the famous quote from US President Thomas Jefferson, "The only security of all is in a free press. The force of public opinion cannot be resisted when permitted freely to be expressed. The agitation it produces must be submitted to. It is necessary, to keep the waters pure."[14] Freedom of the press has long been combated by large media companies, but their objections have just as long been dismissed by the supreme courts.[15]

Recently, new age critical scholarship has emerged that has investigated policymaking critical junctures in the communicative history in northern America. As a result, the media reform movement has flourished. The five core truths have emanated from this movement that analyze and directs progressive forces in this critical juncture.[16]

Deregulation

One explanation for the cause of the concentration of media ownership is a shift to neoliberal deregulation policies, which is a market-driven approach. Deregulation effectively removes governmental barriers to allow for the commercial exploitation of media. Motivation for media firms to merge includes increased profit-margins, reduced risk and maintaining a competitive edge. In contrast to this, those who support deregulation have argued that cultural trade barriers and regulations harm consumers and domestic support in the form of subsidies hinders countries to develop their own strong media firms. The opening of borders is more beneficial to countries than maintaining protectionist regulations.[17]

Critics of media deregulation and the resulting concentration of ownership fear that such trends will only continue to reduce the diversity of information provided, as well as to reduce the accountability of information providers to the public. The ultimate consequence of consolidation, critics argue, is a poorly informed public, restricted to a reduced array of media options that offer only information that does not harm the media oligopoly's growing range of interests.[18]

For those critics, media deregulation is a dangerous trend, facilitating an increase in concentration of media ownership, and subsequently reducing the overall quality and diversity of information communicated through major media channels. Increased concentration of media ownership can lead to corporate censorship affecting a wide range of critical thought.[19]

Other

Another concern is that consolidated media is not flexible enough to serve local communities in case of emergency or that corporate "cost-cutting practices have undermined public safety".[20] For instance, some say that the Minot train derailment was exacerbated by consolidation of media, but the Emergency Alert System (EAS) – which is completely automated once activated – was not activated by emergency management officials because they were not aware that or how they could.[20] After a similar train accident in Macdona, Texas in June 2004, the EAS was again not activated but a commercial radio station in San Antonio provided emergency information as they received it because they were monitoring police scanner traffic.[20][21][22] Another train accident (in Graniteville, S.C., in January of 2005) also resulted in EAS activation failures to the local stations despite their monitoring the appropriate channels.[20] All these incidents indicate that their EAS failures didn't come primarily from consolidated media.[20]

American public distrust in the media

A 2012 Gallup poll found that Americans' distrust in the mass media had hit a new high, with 60% saying they had little or no trust in the mass media to report the news fully, accurately, and fairly. Distrust has steadily increased since 2004, when Americans were already more negative about the media than they had been in years prior.[23]

A recent study has concluded that group participation contributes to the public perceptions of the legitimacy or credibility of mass media. Accordingly, high involvement in media incites more scrutiny and more biased scrutiny of media content.[24]

Media pluralism

The concentration of media ownership is commonly regarded as one of the crucial aspects reducing media pluralism. A high concentration of the media market increases the chances to reduce the plurality of political, cultural and social points of views.[25] Even if ownership of the media is one of the main concerns when it comes to assessing media pluralism, the concept of media pluralism is broader as it touches many aspects, from merger control rules to editorial freedom, the status of public service broadcasters, the working conditions of journalists, the relationship between media and politics, representation of local and regional communities and the inclusion of minorities' voices.[25] Also, it embraces all measures guaranteeing citizens' access to diversified sources so to allow the formation of a plurality of opinions in the public sphere without undue influence of dominant powers.

Furthermore, media pluralism has a two-fold dimension, or rather internal and external. Internal pluralism concerns pluralism within a specific media organisation: in this regard, many countries request public broadcast services to account for a variety of views and opinions, including those of minority groups. External pluralism applies instead to the overall media landscape, for instance in terms of the number of media outlets operating in a given country.[26]

Media ownership can pose serious challenges to pluralism when owners interfere with journalists' independence and editorial line. However, in a free market economy, owners must have the capacity to decide the strategy of their company to remain competitive in the market. Also, pluralism does not mean neutrality and lack of opinion, as having an editorial line is an integral part of the role of editors provided that this line is transparent and explicit to both the staff and audience.[26]

Determinants of media pluralism

Size and wealth of the market

"Within any free market economy, the level of resources available for the provision of media will be constrained principally by the size and wealth of that economy, and the propensity of its inhabitants to consume media." [Gillian Doyle; 2002:15] Those countries that have a relatively large market, like the United Kingdom, France or Spain have more financial background to support diversity of output and have the ability to keep more media companies in the market (as they are there to make profit). More diverse output and fragmented ownership will, obviously, support pluralism. In contrast, small markets like Ireland or Hungary suffer from the absence of the diversity of output given in countries with bigger markets. It means that "support for the media through direct payment" and "levels of consumers expenditure", furthermore "the availability of advertising support" [Gillian Doyle; 2002:15] are less in these countries, due to the low number of audience. Overall, the size and wealth of the market determine the diversity of both media output and media ownership.

Diversity of suppliers/owners

From the previous paragraph it can be assumed that size/wealth of the market have a very strong relation to the diversity of supplier. If the first is not given (wealthy market) then it is difficult to achieve a fragmented supplier system. Diversity of suppliers refers to those heterogeneous independent organizations that are involved in media production and to the common ownership as well. The more various suppliers there are, the better for pluralism is. However, "the more powerful individual suppliers become, the greater the potential threat to pluralism".[27]

Consolidation of resources

The consolidation of cost functions and cost-sharing. Cost-sharing is a common practice in monomedia and cross media. For example, "for multi-product television or radio broadcasters, the more homogeneity possible between different services held in common ownership (or the more elements within a programme schedule which can be shared between 'different' stations), the greater the opportunity to reap economies".[28] Though the main concern of pluralism is that different organization under different ownership may buy the same e.g. news stories from the same news-supplier agency. In the UK, the biggest news-supplier is The Press Association (PA). Here is a quoted text from PA web site: "The Press Association supplies services to every national and regional daily newspaper, major broadcasters, online publishers and a wide range of commercial organisations." Overall, in a system where all different media organizations gather their stories from the same source, we can't really call that system pluralist. That is where diversity of output comes in.[29]

Pluralism in media ownership

Media privatization and the lessening of state dominance over media content has continued since 2012. In the Arab region, the Arab States Broadcasting Union (ASBU) counted 1,230 television stations broadcasting via Arab and international satellites, of which 133 were state-owned and 1,097 private.[30] According to the ASBU Report, these numbers serve as evidence of a decline in the percentage of state channels and a rise in national private and foreign public stations targeting the Arab region. The reduction of direct government ownership over the whole media sector is commonly registered as a positive trend, but this has paralleled by a growth in outlets with a sectarian agenda.[31]

In Africa, some private media outlets have maintained close ties to governments or individual politicians, while media houses owned by politically non-aligned individuals have struggled to survive, often in the face of advertising boycotts by state agencies. In almost all regions, models of public service broadcasting have been struggling for funding. In Western, Central and Eastern Europe, funds directed to public service broadcasting have been stagnating or declining since 2012.[32]

New types of cross-ownership have emerged in the past five years that have spurred new questions about where to draw the line between media and other industries. A notable case has been the acquisition of the Washington Post by the founder of online retailer Amazon. While the move initially raised concerns about the newspaper's independence, the newspaper has significantly increased its standing in the online media—and print—and introduced significant innovations.[31]

The community-centred media ownership model continues to survive in some areas, especially in isolated, rural or disadvantaged areas, and mostly pertaining to radio. Through this model, not-for-profit media outlets are run and managed by the communities they serve.[31]

Newspaper and Advertising

Media ownership avoid news which is critical of advertisers. Cater to the interests of prized demographics. Producing news which puts audiences in a "buying mood" as consumers.

In particular nations

Australia

Controls over media ownership in Australia are laid down in the Broadcasting Services Act 1992,[33] administered by the Australian Communications and Media Authority (ACMA). Even with laws in place Australia has a high concentration of media ownership. Ownership of national and the newspapers of each capital city are dominated by two corporations, Rupert Murdoch's News Corp Australia, (which was founded in Adelaide as News Limited) and Nine Entertainment Co.. These two corporations along with Seven West Media co-own Australian Associated Press which distributes the news and then sells it on to other outlets such as the Australian Broadcasting Corporation. Although much of the everyday mainstream news is drawn from the Australian Associated Press, all the privately-owned media outlets still compete with each other for exclusive pop culture news. Rural and regional media is dominated by Australian Community Media, with significant holdings in all states and territories. Daily Mail and General Trust operate the DMG Radio Australia commercial radio networks in metropolitan and regional areas of Australia. Formed in 1996, it has since become one of the largest radio media companies in the country. The company currently own more than 60 radio stations across New South Wales, Victoria, South Australia, Queensland and Western Australia.

There are rules governing foreign ownership of Australian media and these rules were loosened by the former Howard Government.

According to Reporters Without Borders in 2004, Australia is in 41st position on a list of countries ranked by Press Freedom; well behind New Zealand (9th) and United Kingdom (28th). This ranking is primarily due to the limited diversity in media ownership. By 2013, Australia had risen to 26th on the Press Freedom Index.

Media Watch is an independent media watchdog televised on the public broadcaster Australian Broadcasting Corporation (ABC), which is one of two government-administered channels, the other being Special Broadcasting Service (SBS).

In late 2011, the Finkelstein Inquiry into media regulation was launched, and reported its findings back to the federal government in early 2012.[34]

New Zealand

Independent Newspapers Limited (INL) formerly published the Wellington-based newspapers The Dominion and The Evening Post, in addition to purchasing a large shareholding in pay TV broadcaster Sky Media Limited in 1997. These two newspapers merged to form the Dominion Post in 2002, and in 2003, sold its entire print media division to Fairfax New Zealand. The remainder of the company officially merged with Sky Media Limited in 2005 to form Sky Network Television Limited.

When INL ceased publishing the Auckland Star in 1991, The New Zealand Herald became the Auckland region's sole daily newspaper. The New Zealand Herald and the New Zealand Listener, formerly privately held by the Wilson & Horton families, was sold to APN News & Media in 1996. The long-running news syndication agency NZPA announced that it would close down in 2011, with operations to be taken over by 3 separate agencies, APN's APNZ, Fairfax's FNZN and AAP's NZN, all owned by Australian parent companies.[35] In 2014, APN's New Zealand division officially changed its name to NZME, in order to reflect the company's convergence with its radio division The Radio Network. As of early 2015, Fairfax New Zealand and NZME have a near duopoly on newspapers and magazines in New Zealand. In May 2016, NZME and Fairfax NZ announced merger talks, pending Commerce Commission approval.[36]

Commercial radio stations are largely divided up between MediaWorks New Zealand and NZME, with MediaWorks also owning TV3 and C4 (now The Edge TV). Television New Zealand, although 100% state-owned, has been run on an almost entirely commercial basis since the late 1980s, in spite of previous attempts to steer it towards a more public service-oriented role. Its primary public-service outlet, TVNZ7, ceased broadcasting in 2012 due to non-renewal of funding, and the youth-oriented TVNZ6 was rebranded as the short-lived commercial channel TVNZ U. In addition, the TVNZ channels Kidzone (and formerly TVNZ Heartland) are only available through Sky Network Television and not on the Freeview platform.[37]

Sky Network Television has had an effective monopoly on pay TV in New Zealand since its nearest rival Saturn Communications (later part of TelstraClear and now Vodafone New Zealand) began wholesaling Sky content in 2002. However, in 2011, TelstraClear CEO Allan Freeth warned it would review its wholesale agreement with Sky unless it allowed TelstraClear to purchase non-Sky content.[38]

Canada

Canada has the biggest concentrated TV ownership out of all the G8 countries and it comes in second place for the most concentrated television viewers.[39]

Broadcasting and telecommunications in Canada are regulated by the Canadian Radio-television and Telecommunications Commission (CRTC), an independent governing agency that aims to serve the needs and interests of citizens, industries, interest groups and the government. The CRTC does not regulate newspapers or magazines.[40]

Apart from a relatively small number of community broadcasters, media in Canada are primarily owned by a small number of groups, including Bell Canada, the Shaw family (via Corus Entertainment and Shaw Communications), Rogers Communications, Quebecor, and the government-owned CBC/Radio-Canada. Each of these companies holds a diverse mix of television, specialty television, and radio operations. Bell, Rogers, Shaw, and Quebecor also engage in the telecommunications industry with their ownership of internet providers, television providers, and mobile carriers, while Rogers is also involved in publishing.

In 2007, CTVglobemedia, Rogers Media and Quebecor all expanded significantly through the acquisitions of CHUM Limited, CityTV and Osprey Media, respectively. In 2010, Canwest Global Communications, having filed for bankruptcy, sold its television assets to Shaw (through a new subsidiary, Shaw Media) and spun off its newspaper holdings into Postmedia Network, a new company founded by the National Post's CEO Paul Godfrey.[41] Later that year, Bell also announced that it would acquire the remaining shares of CTVglobemedia (which was originally majority owned by Bell when it was formed in 2001; Bell had reduced its stake in the following years), forming Bell Media.[42]

Between 1990 and 2005 there were a number of media corporate mergers and takeovers in Canada. For example, in 1990, 17.3% of daily newspapers were independently owned; whereas in 2005, 1% were.[43] These changes, among others, caused the Senate Standing Committee on Transport and Communications to launch a study of Canadian news media in March 2003. (This topic had been examined twice in the past, by the Davey Commission (1970) and the Kent Commission (1981), both of which produced recommendations that were never implemented in any meaningful way.)[44][45]

The Senate Committee's final report, released in June 2006, expressed concern about the effects of the current levels of news media ownership in Canada. Specifically, the committee discussed their concerns regarding the following trends: the potential of media ownership concentration to limit news diversity and reduce news quality; the CRTC and Competition Bureau's ineffectiveness at stopping media ownership concentration; the lack of federal funding for the CBC and the broadcaster's uncertain mandate and role; diminishing employment standards for journalists (including less job security, less journalistic freedom, and new contractual threats to intellectual property); a lack of Canadian training and research institutes; and difficulties with the federal government's support for print media and the absence of funding for the internet-based news media.[44][45]

The Senate report expressed particular concern about the concentration of ownership in the province of New Brunswick, where the Irving business empire owns all the English-language daily newspapers and most of the weeklies. Senator Joan Fraser, author of the report, stated, "We didn't find anywhere else in the developed world a situation like the situation in New Brunswick."[46]

The report provided 40 recommendations and 10 suggestions (for areas outside of federal government jurisdiction), including legislation amendments that would trigger automatic reviews of a proposed media merger if certain thresholds are reached, and CRTC regulation revisions to ensure that access to the broadcasting system is encouraged and that a diversity of news and information programming is available through these services.[44][45]

Public inquires into the concentration of ownership and its impact upon democracy. The Canadian regulatory framework imposes requirements upon the protection and enhancement of Canadian culture (through regulation, subsidies and the operation of the CBC). Increasing acceptance of media/news as commercial enterprise in 1990s driven by: hegemony of new-liberalism, role of commodified information technology in economic growth, commitment to private sector "champions" of Canadian culture.

Brazil

In Brazil, the concentration of media ownership seems to have manifested itself very early. Dr. Venício A. de Lima noted in 2003:

It must be noted that in Brazil there is an environment very conducive to concentration. Sectorial legislation has been timid, by express intention of the legislator, by failing to include direct provisions that limit or control the concentration of ownership, which, incidentally, goes in the opposite direction of what happens in countries like France, Italy and the United Kingdom, which are concerned with the plurality and diversity in the new scenario of technological convergence.

Lima points to other factors that would make media concentration easier, particularly in broadcasting: the failure of legal norms that limit the equity interest of the same economic group in various broadcasting organizations; a short period (five years) for resell broadcasting concessions, facilitating the concentration by the big media groups through the purchase of independent stations, and no restrictions to the formation of national broadcasting networks. He cites examples of horizontal, vertical, crossed and "in cross" concentration (a Brazilian peculiarity).[47]

- Horizontal concentration: oligopoly or monopoly produced within an area or industry; television (pay or free) is the Brazilian classical model. In 2002 the cable networks Sky and NET dominated 61% of the Brazilian market. In the same year, 58.37% of all advertising budgets were invested in TV – and in this aspect, TV Globo and its affiliates received 78% of the amount.[48]

- Vertical concentration: integration of the different phases of production and distribution, eliminating the work of independent producers. In Brazil, unlike the United States, it is common for a TV network to produce, advertise, market and distribute most of its programming. TV Globo is known for its soap operas exported to dozens of countries; it keeps under permanent contract the actors, authors, and the whole production staff. The final product is broadcast by a network of newspapers, magazines, radio stations and websites owned by Globo Organizations.[49]

- Cross ownership: ownership of different kinds of media (TV, newspapers, magazines, etc.) by the same group. Initially, the phenomenon occurred in radio, television and print media, with emphasis on the group of "Diários Associados." At a later stage appeared the RBS Group (affiliated to TV Globo), with operations in the markets of Rio Grande do Sul and Santa Catarina. Besides being the owner of radio and television stations, and of the main local newspapers, it has two Internet portals. The opinions of its commentators are thus replicated by a multimedia system that makes it extremely easy to spread the point of view advocated by the group.[50][51]

- Monopoly "in cross": reproduction into local level, of the particularities of cross ownership. Research carried out in the early 1990s, detected the presence of this singularity in 18 of the 26 Brazilian states.[52] Manifests itself by the presence of a TV channel with a large audience, often linked to TV Globo and by the existence of two daily newspapers, in which the one with the largest circulation is linked to the major television channel and to a network of radio stations, that almost always reproduces articles and the editorial line of the newspaper "O Globo".[53] In 2002, another survey (which did not include pay TV), found the presence of the "monopoly in cross" in 13 major markets in Brazil.[54]

The UNESCO office in Brasília has expressed its concern over the existence of an outdated code of telecommunications (1962),[55] which no longer meets the expectations generated by the Brazilian Constitution of 1988 in the political and social fields, and the inability of the Brazilian government to establish an independent regulatory agency to manage the media.[56] Attempts in this direction have been pointed by the mainstream media as attacks on freedom of expression, the trend of the political left in the entire Latin American continent.[57][58][59][60]

Europe

Council of Europe and European Union

Since the 1980, a significant debate has developed at the European level concerning the regulation of media ownership and the principles to be adopted to regulate media ownership concentration.[61] Both the Council of Europe (CoE) and the European Union (EU) have tried to formulate a distinctive and comprehensive media policy, including on the issue of concentration.[62] However, the emphasis of both the organisations was more on strengthening media diversity and pluralism than on limiting concentration, even though they have often expressed the need for common European media concentration regulations.[62] However, the European Union enforces a common regulation for environmental protection, consumer protection and human rights, but it has none for media pluralism.[63]

Although there is no specific media concentration legislation at the European level, a number of existing legal instruments such as the Amsterdam Protocol, the Audiovisual Media Services Directive and actions programs contribute directly and indirectly to curbing media concentration at EU level.[62]

When it comes to regulating media concentration at the common European level, there is a conflict between Member states and the European Commission (EC). Even if Member states do not publicly challenge the need for common regulation on media concentration, they push to incorporate their own regulatory approach at the EU level and are reluctant to give the European Union their regulatory power on the issue of media concentration.[62]

The Council of Europe's initiative promoting media pluralism and curbing media concentration dates back to the mid-1970s. Several resolutions, recommendations, declarations by the Council of Europe Committee of Ministers and studies by experts' groups have addressed the issue since then.[62] The Council's approach has been mainly addressed at defining and protecting media pluralism, defined in terms of pluralism of media content in order to allow a plurality of ideas and opinions.[62]

Within the European Union, two main standpoints have emerged in the debate: on the one hand, the European Parliament has favoured the idea that, considering the crucial role that media play in the functioning of democratic systems, policies in this field should prevent excessive concentration in order to guarantee pluralism and diversity. On the other hand, the European Commission has privileged the understanding that the media sector should be regulated, as any other economic field, following the principles of market harmonization and liberalization.[61]

Indeed, media concentration issues can be addressed both by general competition policies and by specific media sector rules. According to some scholars, given the vital importance of contemporary media, sector-specific competition rules in the media industries should be enhanced.[62] Within the EU, the Council regulation 4064/89/EEC on the control of concentrations between undertakings as part of European competition legislation covered also media concentration cases.[62] The need for sector-specific regulation has been widely supported by both media scholars and the European Parliament. In the 1980s, when preparing legislation on cross-border television many experts and MEPs argued for including provisions for media concentration in the EU directive but these efforts failed.[62] In 1992, the Commission of the European Communities published a policy document named "Pluralism and Media Concentration in the internal Market – an assessment of the need for Community action" which outlined three options on the issue of media concentration regulation at the Community level, i.e. no specific action to be taken; action regulating transparency; and action to harmonize laws. Out of these options, the first one was chosen but the debate on this decision lasted for years.[62] Council regulation as a tool for regulating media concentration was excluded and the two proposals on a media concentration directive advanced in the mid 1990s were not backed by the Commission. As a consequence, efforts at legislating media concentration at Community level were phased out by the end of the 1990s.[62]

Despite a wide consensus over the idea that the vital importance of contemporary media justifies to regulate media concentration through sector-specific concentration rules going beyond the general competition policy, the need for sector specific regulation has been challenged in recent years due to the peculiar evolution of the media industry in the digital environment and media convergence. In practice, sector-specific media concentration rules have been abolished in some European countries in recent years.[62]

As a consequence, scholars Harcourt and Picard argue that "the trend has been to remove ownership rules and restrictions on media ownership within Europe in order that 'domestic champions' can bulk up to 'fend off' the US threat. This has been a key argument for the loosening of ownership rules within Europe."[64]

In 2002, the European Parliament tried to revitalize the efforts on regulating media concentration at the European level and adopted a resolution on media concentration which called on the European Commission to launch a broad and comprehensive consultation on media pluralism and media concentration and to prepare a Green Paper on the issue by the end of 2003. The European Commission failed to meet this deadline.[62] In the following years, during the process of amending the Televisions Without Frontiers directive, which was adopted by the EP and the Council in 2007, the issue of media concentration was discussed, but it did not represented the core of the debate.[62] In 2003, the European Commission issued a policy document named "The future of European Regulatory Audiovisual Policy" which stressed that, in order to ensure media pluralism, measures should aim at limiting the level of media concentration by establishing "maximum holdings in media companies and prevent[ing] cumulative control or participation in several media companies at the same time".[62]

In 2007, reacting to concerns on media concentration and its repercussion on pluralism and freedom of expression in the EU member states raised by the European Parliament and by NGOs, the European Commission launched a new three-phase plan on media pluralism[63][65][66]

In October 2009, a European Union Directive was proposed to set for all member states common and higher standards for media pluralism and freedom of expression. The proposal was put to a vote in the European Parliament and rejected by just three votes. The directive was supported by the liberal-centrists, the progressives and the greens, and was opposed by the European People's Party.[63] Unexpectedly, the Irish liberals made an exception by voting against the directive, and later revealed that they had been pressured by the Irish right-wing government to do so.[63]

Following this debate, the European Commission commissioned a large, in depth study published in 2009 aiming to identify the indicators to be adopted to assess media pluralism in Europe.[67]

The "Independent Study on Indicators for Media Pluralism in the Member States – Towards a Risk-Based Approach" provided a prototype of indicators and country reports for 27 EU member states. After years of refining and preliminary testings, the study resulted in the Media Pluralism Monitor (MPM), a yearly monitoring carried out by the Centre for media pluralism and freedom at the European University Institute in Florence on a variety of aspects affecting media pluralism, including also the concentration of media ownership is considered.[68] To assess the risk that media ownership concentration in a given country may actually hinder media pluralism, the MPM takes into account three specific elements:

- Horizontal concentration, that is concentration of media ownership within a given media sector (press, audio-visual, etc.);

- Cross-media concentration across different media markets;

- Transparency of media ownership.

In 2015, the MPM was carried out in 19 European countries. The results of the monitoring activity in the field of media market concentration identify five countries as facing a high risk: Finland, Luxembourg, Lithuania, Poland and Spain. There are nine countries facing a medium risk: Czech Republic, Germany, Ireland, Latvia, Netherlands, Portugal, Romania, Sweden. Finally, only five countries face a low risk: Croatia, Cyprus, Malta, Slovenia and Slovakia.[69] In the monitoring carried out in 2014, 7 of 9 countries (Belgium, Bulgaria, Denmark, France, Hungary, Italy, the UK) scored a high risk in audience concentration.[70]

Pan-European groups

A 2016 report based on data collected by MAVISE, a free online database on audiovisual services and companies in Europe, highlights the growing number of Pan-European media companies in the field of broadcasting and divides them into different categories: multi‐country media groups, controlling “channels that play an important role in various national markets (for example Modern Times Group, CEME, RTL, a Luxembourg-based media group operating in 10 countries,[71] and Sanoma). These groups generally control a high market share in the countries in which they operate, and have gradually emerged through the acquisition of existing channels or by establishing new companies in countries in which they were not already present.[72] The four groups RTL Group, CEME, Modern Times Group and Sanoma are major players (in the top 4 regarding audience share) in 19 European countries (RTL Group, CEME and Modern Times Group are major players in 17 countries).[72] Pan‐European broadcasters operate with a unique identity and well recognized brands across Europe. Most of them are based in the United States and have progressively expanded their activities in the European market. In many cases, these groups evolved from being content creators to also deliver such contents through channels renamed after the original brands.

Examples of such pan-European groups include Discovery, ViacomCBS, WarnerMedia, and The Walt Disney Company,[72] pan‐European distribution groups (cable and satellite operators), companies that operate at the European level in the distribution sector via cable, satellite or IPTV. The emergence of major actors operating in this field has been made possible mainly thanks to the process of digitalization and benefit of specific economies of scale.[72]

EU Member States

Czech Republic

In the Czech Republic about 80% of the newspapers and magazines were owned by German and Swiss corporations in 2007,[73] as the two main press groups Vltava Labe Media and Mafra were (completely or partly) controlled by the German group Rheinisch-Bergische Druckerei- und Verlagsgesellschaft (Mediengruppe Rheinische Post), but were both later purchased by Czech-owned conglomerates Penta Investments and Agrofert in 2015 and 2013 respectively. Several major media previously owned by Swiss company Ringier became Czech-owned through their acquisition by the Czech News Center in 2013.

- Vltava Labe Media, a subsidiary of Penta Investments, that owns the tabloids ŠÍP and ŠÍP EXTRA, 73 regional dailies Deník and other 26 weeklies[74][75] and that is major shareholder of publishing houses Astrosat and Melinor[76][77] and 100% owner of Metropol[78] and also partly controls the distribution of all the prints through PNS, a.s.[79] which was previously part of the German Verlagsgruppe Passau[80] (that controls also the German Neue Presse Verlags, the Polish Polskapresse and the Slovak Petit Press).[81]

- Mafra, a subsidiary of Agrofert (that owns the centre-right dailies Dnes, Lidové noviny,[82] the local edition of the freesheet Metro, the periodical 14dní, several monthly magazines, the TV music channel Óčko, the radio stations Expresradio and Rádio Classic FM, several web portals[83][84] and partly controls, together with Vltava-Labe-Press, the distribution company PNS, a.s.)[79] was previously owned by the German Rheinisch-Bergische Drückerei- und Verlagsgesellschaft, prior to its acquisition by Agrofert.

- Czech News Center controls 16 Czech daily tabloids and weeklies (such as 24 hodin, Abc, Aha!, Blesk, Blesk TV Magazin, Blesk pro ženy, Blesk Hobby, Blesk Zdravi, Nedělní Blesk, Nedělní Sport, Reflex, Sport, Sport Magazin) as well as 7 web portals, reaching approximately 3.2 million readers.

Czech governments have defended foreign newspaper ownership as a manifestation of the principle of the free movement of capital.[85]

The weekly Respekt is published by R-Presse, the majority of whose shares are owned by former Czech Minister of Foreign Affairs Karel Schwarzenberg.[85] The national television market is dominated by four terrestrial stations, two public (Czech TV1 and Czech TV2) and two private (NOVA TV and Prima TV), which draw 95% of audience share.[86] Concerning the diversity of output, this is limited by a series of factors: the average low level of professional education among Czech journalists is compensated by "informal professionalization", leading to a degree of conformity in approaches;[87] political parties hold strong ties in Czech media, especially print, where more than 50% of Czech journalists identify with the Right, while only 16% express sympathy for the Left;[87] and the process of commercialization and "tabloidization" has increased, lowering differentiation of content in Czech print media.[87]

Germany

Axel Springer AG is one of the largest newspaper publishing companies in Europe, claiming to have over 150 newspapers and magazines in over 30 countries in Europe. In the 1960s and 1970s the company's media followed an aggressive conservative policy (see Springerpresse). It publishes Germany's only nationwide tabloid, Bild, and one of Germany's most important broadsheets, Die Welt. Axel Springer also owns a number of regional newspapers, especially in Saxony and in the Hamburg Metropolitan Region, giving the company a de facto monopoly in the latter case. An attempt to buy one of Germany's two major private TV Groups, ProSiebenSat.1, in 2006, was withdrawn due to large concerns by regulation authorities as well as by parts of the public. The company is also active in Hungary, where it is the biggest publisher of regional newspapers, and in Poland, where it owns the best-selling tabloid Fakt, one of the nation's most important broadsheets, Dziennik, and is one of the biggest shareholder in the second-ranked private TV company, Polsat.

Bertelsmann is one of the world's largest media companies. It owns RTL Group, which is one of the two major private TV companies in both Germany and the Netherlands and also owning assets in Belgium, France, UK, Spain, Czech and Hungary. Bertelsmann also owns Gruner + Jahr, Germany's biggest popular magazine publisher, including popular news magazine Stern and a 26% share in investigative news magazine Der Spiegel. Bertelsmann also owns Random House, a book publisher, ranked first in the English-speaking world and second in Germany.

Ireland

In Ireland, the company Independent News & Media owns many national newspapers: the Evening Herald, Irish Independent, Sunday Independent, Sunday World and Irish Daily Star. It also owns 29.9% of the Sunday Tribune. Broadcast media is divided between state owned RTÉ, which operates several radio stations and television channels and started digital radio and television services in the early 2010s, TG4, an Irish language broadcaster, and TV3, a commercial television operator. Denis O'Brien an Irish billionaire with a fortune partly accumulated through the Esat Digifone licence controversy, formed Communicorp Group Ltd in 1989, with the company currently owning 42 radio stations in 8 European countries, including Ireland's Newstalk, Today FM, Dublin's 98FM, SPIN 1038 and SPIN South West. In January 2006, O'Brien took a stake in Tony O'Reilly's Independent News & Media (IN&M). As of May 2012, he holds a 29.9% stake in the company, making him the largest shareholder; the O'Reilly family's stake is around 13%.

Italy

Silvio Berlusconi, the former Prime Minister of Italy, is the major shareholder of – by far – Italy's biggest (and de facto only) private free TV company, Mediaset; Italy's biggest publisher, Mondadori; and Italy's biggest advertising company, Publitalia. One of Italy's nationwide dailies, Il Giornale, is owned by his brother, Paolo Berlusconi, and another, Il Foglio, by his former wife, Veronica Lario. Berlusconi has often been criticized for using the media assets he owns to advance his political career.

United Kingdom

In Britain and Ireland, Rupert Murdoch owns best-selling tabloid The Sun as well as the broadsheet The Times and Sunday Times, and 39% of satellite broadcasting network BSkyB. In March 2011, the United Kingdom provisionally approved Murdoch to buy the remaining 61% of BSkyB;[88] however, subsequent events (News of the World hacking scandal and its closure in July 2011) leading to the Leveson Inquiry have halted this takeover.

Trinity Mirror own five major national titles, the Daily Mirror, Sunday Mirror and The Sunday People, and the Scottish Sunday Mail and Daily Record as well as over 100 regional newspapers. They claim to have a monthly digital reach of 73 million people.

Daily Mail and General Trust (DMGT) own the Daily Mail and The Mail on Sunday, Ireland on Sunday, and free London daily Metro, and control a large proportion of regional media, including through subsidiary Northcliffe Media, in addition to large shares in ITN and GCap Media.

The Guardian is owned by Guardian Media Group.

Richard Desmond owns OK! magazine, the Daily Express, and the Daily Star. He used to own Channel 5; on 1 May 2014 the channel was acquired by Viacom for £450 million (US$759 million).

The Evening Standard[89] and former print publication The Independent[90] are both partly owned by British-Russian media boss Evgeny Lebedev.

BBC News produces news for its television channels and radio stations.

Independent Television News produces news for ITV, Channel 4 and Channel 5.

Independent Radio News, which has a contract with Sky News, produces news for the most popular commercial radio stations.

India

In India a few political parties also own media organizations, for example the proprietors of Kalaignar TV are close aides of Tamil Nadu's former Chief Minister M. Karunanidhi. So is also the case with Sun TV. SRM university owner Pachamuthu, a member of Parliament, has stakes in Pudhiyathalaimurai News Channel. AMMK General Secretary TTV Dinakaran, MLA's close aides run Jaya Tv. Sakshi TV a Telugu channel in Andhra Pradesh is owned by ex-chief minister's son and family.

India passed legislation in July of 2018 that demands net neutrality and an open and fair network access for all citizens of India, [91] This ensures the right of access to internet to over 1,376,000,000 people.

Israel

In Israel, Arnon Mozes owns the most widespread Hebrew newspaper, Yediot Aharonot, the most widespread Russian newspaper Vesty, the most popular Hebrew news website Ynet, and 17% of the cable TV firm HOT. Moreover, Mozes owns the Reshet TV firm, which is one of the two operators of the most popular channel in Israel, Channel 2.[92]

Mexico

In Mexico there are only two national broadcast television service companies, Televisa and Azteca. These two broadcasters together administer 434 of the 461 total commercial television stations in the country (94.14%).[93]

Though concern about the existence of a duopoly had been around for some time, a press uproar sparked in 2006, when a controversial reform to the Federal Radio and Television Law, seriously hampered the entry of new competitors, like Cadena Tres.[94]

Televisa also owns subscription TV enterprises Cablevision (Mexico) and SKY, a publishing company Editorial Televisa, and the Televisa Radio broadcast radio network, creating a de facto media monopoly in many regions of the country.

United States

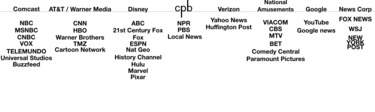

In the United States, movie production has been dominated by major studios since the early 20th century; before that, there was a period in which Edison's Trust monopolized the industry. The music and television industries recently witnessed cases of media consolidation, with Sony Music Entertainment's parent company merging their music division with Bertelsmann AG's BMG to form Sony BMG and Tribune's The WB and CBS Corp.'s UPN merging to form The CW. In the case of Sony BMG, there existed a "Big Five" (now "Big Four") of major record companies, while The CW's creation was an attempt to consolidate ratings and stand up to the "Big Four" of American network (terrestrial) television (this despite the fact that the CW was, in fact, partially owned by one of the Big Four in CBS). In television, the vast majority of broadcast and basic cable networks, over a hundred in all, are controlled by eight corporations: Fox Corporation, The Walt Disney Company (which includes the ABC, ESPN, FX and Disney brands), National Amusements (which owns ViacomCBS), Comcast (which owns NBCUniversal), AT&T (which owns WarnerMedia), Discovery, Inc., E. W. Scripps Company, Cablevision (now known as Altice USA), or some combination thereof.[95]

There may also be some large-scale owners in an industry that are not the causes of monopoly or oligopoly. iHeartMedia (formerly Clear Channel Communications), especially since the Telecommunications Act of 1996, acquired many radio stations across the United States, and came to own more than 1,200 stations. However, the radio broadcasting industry in the United States and elsewhere can be regarded as oligopolistic regardless of the existence of such a player. Because radio stations are local in reach, each licensing a specific part of spectrum from the FCC in a specific local area, any local market is served by a limited number of stations. In most countries, this system of licensing makes many markets local oligopolies. The similar market structure exists for television broadcasting, cable systems and newspaper industries, all of which are characterized by the existence of large-scale owners. Concentration of ownership is often found in these industries.

In the United States, data on ownership and market share of media companies is not held in the public domain.

Effect of ownership on coverage

Organizations like Fairness and Accuracy in Reporting have accused the Military-industrial-media complex of using their media resources to promote militarism, which, according to Fairness and Accuracy in Reporting's hypothesis, benefits the defense resources of the company. As FAIR observed, "when correspondents and paid consultants on NBC television praised the performance of U.S. weapons, they were extolling equipment made by GE, the corporation that pays their salaries."[96]

Recent media mergers in the United States

Over time the amount of media merging has increased and the number of media outlets has increased. As a result, fewer companies now own more media outlets, increasing the concentration of ownership.[7] In 1983, 90% of US media was controlled by 50 companies; as of 2011, 90% was controlled by just 6 companies and in 2017 the number was 5.[97]

Top Five

| Company | Media Outlets | Revenues (2018) |

|---|---|---|

| AT&T | Holdings include: WarnerMedia (CNN, The CW (a joint venture with CBS), HBO, Cinemax, Cartoon Network, Adult Swim, HLN, NBA TV, TBS, TNT, TruTV, Turner Classic Movies, AT&T SportsNet, Audience, Otter Media, Warner Bros. Pictures, Castle Rock, DC Comics, Warner Bros. Interactive Entertainment, and New Line Cinema), DirecTV, U-Verse, other channels, AT&T Mobility and Cricket Wireless. | |

| Comcast | Holdings include: NBCUniversal, NBC and Telemundo, Universal Pictures, Illumination Entertainment, Focus Features, DreamWorks Animation, 26 television stations in the United States and cable networks USA Network, Bravo, CNBC, MSNBC, Syfy, NBCSN, Golf Channel, E!, and NBC Sports Regional Networks. Comcast also owns the Philadelphia Flyers through a separate subsidiary. | |

| The Walt Disney Company | Holdings include: ABC Television Network, cable networks ESPN, the Disney Channel, Disney XD, Freeform, FX, FXX, FX Movie Channel, National Geographic, Nat Geo Wild, History, A&E and Lifetime, approximately 30 radio stations, music, video game, and book publishing companies, production companies Blue Sky Studios, 20th Century Fox, Fox Searchlight Pictures, Touchstone, Marvel Entertainment, Lucasfilm, Walt Disney Pictures, Pixar Animation Studios, mobile app developer Disney Mobile, Disney Consumer Products and Interactive Media, and theme parks in several countries.

See: List of assets owned by Disney. |

|

| ViacomCBS | Holdings include: CBS Television Network and the CW (a joint venture with WarnerMedia via AT&T), Paramount Pictures, Paramount Home Media Distribution, cable networks BET, CBS Sports Network, Showtime, CMT, Comedy Central, Logo TV, MTV, Nickelodeon/Nick at Nite, Paramount Network, Pop, TV Land, VH1; 30 television stations; CBS Television Studios; book publisher Simon & Schuster. | US$27.45 billion (combined revenue from Viacom and CBS Corporation)[101][102] |

| Fox Corporation | Holdings include: Fox Broadcasting Company, Fox News Group (Fox News Channel, Fox Business Network, Fox News Radio, Fox News Talk, Fox Nation), Fox Sports (FS1, FS2, Fox Deportes, Big Ten Network (51%), Fox Sports Radio) |

*Before the second merger of Viacom and CBS, CBS has also recently spun off its radio assets, causing them to merge with Entercom.

News Corporation was split into two separate companies on June 28, 2013, with publishing assets and Australian media assets going to a spin-off known as News Corp, and broadcasting and media assets going to 21st Century Fox. Both companies remain under the control of Rupert Murdoch, although Murdoch has reduced involvement in the new News Corp.[104] Most of 21st Century Fox's properties are now owned by the Walt Disney Company (through their acquisition of the company), while others have gone into the newly founded Fox Corporation, or sold to other companies.

Venezuela

About 70% of Venezuelan TV and radio stations are privately owned, while only about 5% or less of these stations are currently state-owned. The remaining stations are mostly community owned. VTV was the only state TV channel in Venezuela only about a decade ago. For the last decade, through the present day, the Venezuelan government operates and owns five more stations.[105]

Commercial outlets completely rule over the radio sector. However, the Venezuelan government funds a good number of radio shows and TV stations. The primary newspapers of Venezuela are private companies that are frequently condemning of their government. These newspapers being produced in Venezuela do not have a large following.[105]

See also

- Agenda-setting theory

- Alternative media

- Big Three television networks

- Corporate media

- Deregulation

- Freedom of speech

- Freedom of the press

- Gleichschaltung

- Lists of corporate assets

- Local News Service

- Mainstream

- Mainstream media

- Media bias

- Media conglomerate

- Media cross-ownership in the United States

- Media democracy

- Media imperialism

- Media manipulation

- Media proprietor

- Media transparency

- Monopolies of knowledge

- Network neutrality

- Old media

- Partido da Imprensa Golpista

- Politico-media complex

- Prometheus Radio Project

- Propaganda model

- Retail concentration

- State controlled media

- Telecommunications Act of 1996

- Western media

- Transparency of media ownership in Europe

Sources

![]()

Notes

- Steven, 2009: p. 19

- Downing, John, ed. (2004). The SAGE Handbook of Media Studies. SAGE. p. 296. ISBN 978-0-7619-2169-1.

- Lorimer, Rowland; Scannell, Paddy (1994). Mass communications: a comparative introduction. Manchester University Press. pp. 86–87. ISBN 978-0-7190-3946-1.

- "Global Media". New Internationalist. April 2001. Retrieved 2009-10-10.

- "Ultra Concentrated Media - Facts". New Internationalist. April 2001. Retrieved 2009-10-10.

- Katharine Ainger (April 2001). "Empires of the Senseless". New Internationalist. Retrieved 2009-10-10.

- "Media Conglomerates, Mergers, Concentration of Ownership". Retrieved 9 January 2016.

- Woodhull, Nancy J.; Snyder, Robert W., eds. (2020-03-24). "Media Mergers". doi:10.4324/9781351309363. Cite journal requires

|journal=(help) - Straubhaar, Joseph, Robert LaRose, and Lucinda Davenport. Media Now: Understanding Media, Culture, and Technology. Wadsworth Pub Co, 2008. Print.

- Petković, Brankica (2015). Media Integrity Matters: Understanding the Meaning of and Risks to Media Integrity. Ljubljana: Peace Institute.

- "CNN American Morning Sells Out Cancer Survivor for Coal". YouTube. Retrieved 2013-04-30.

- Lee Plaisance, Patrick (June 2016). "Journalism Ethics". Oxford Research Encyclopedia of Communication. doi:10.1093/acrefore/9780190228613.013.89. ISBN 9780190228613.

- von Dohnanyi, Johannes (2003). "The Impact of Media Concentration on Professional Journalism". Organization for Security and Co-operation in Europe /OSCE.

- "Government: Watchdog Organizations". Activism. 1999-02-22. Retrieved 2013-04-30.

- Baker, C. Edmund (2007). Media concentration and democracy: why ownership matters. New York; Cambridge: Cambridge University Press. p. 127.

- Barron, Jerome A. "Freedom of the Press for Whom? The Question to be Answered in our Critical Juncture."Freedom of the Press for Whom? the Right of Access to Mass Media. Bloomington: Indiana UP, 1973. N. pag. Print.

- McChesney, R. (2001). "Global media, neoliberalism and imperialism". Monthly Review. 52 (10): 1. doi:10.14452/MR-052-10-2001-03_1.

- Baker, C. Edmund (2007). Media concentration and democracy: why ownership matters. New York; Cambridge: Cambridge University Press. p. 3.

- Cooper, M. (2004). "Limits on Media Ownership Serve the Public Interest". Television Quarterly. 34 (3/4).

- Mustoe, M (2006-01-18). "Commentary: Reconsidering Minot and EAS". Radio World. Archived from the original on 2013-01-21. Retrieved 15 February 2020.

- "DEFINING LOCALISM'S ROLE IN PUBLIC WARNING RADIO (Part III of Mustoe 2005 paper at AAG)". Archived from the original on 2007-11-08.

- Mustoe, M (8 April 2005). "The Emergency Alert System: Its Viability in the New Localism of Commercial Radio". Eastern Oregon University. Archived from the original on 26 April 2007. Retrieved 15 February 2020.

Presented at the Annual Meeting of the American Association of Geographers Denver Meeting 8 April 2005

- "U.S. Distrust in Media Hits New High". Gallup. September 21, 2012.

- Gunther, Albert C. (1992). Biased Press or Biased Public? Attitudes Toward Media Coverage of Social Groups. Public Opinion Quarterly.

- "Monitoring media pluralism in Europe : testing and implementation of the media pluralism monitor 2014" (PDF).

- A Free and pluralistic media to sustain European democracy. The report of the High Level Group on Media Freedom and Pluralism, European Commission, January 2013. Retrieved 14 June 2016.

- Doyle, 2002: p. 18

- Doyle, 2002: p. 22–23

- Doyle, Gillian (2002). "What's "new" about the future of communications? An evaluation of recent shifts in UK media ownership policy". 24 (5). Cite journal requires

|journal=(help) - Arab States Broadcasting Union. 2015. Arab Satellite Broadcasting Annual Report 2015. Available at <http://www.asbu.net/medias/ NewMedia_2016/text/asbu_report_2015. pdf>.

- World Trends in Freedom of Expression and Media Development Global Report 2017/2018. http://unesdoc.unesco.org/images/0026/002610/261065e.pdf: UNESCO. 2018. p. 202.CS1 maint: location (link)

- European Broadcasting Union (EBU). 2015. Funding of Public Service Media 2015. Available at <https://www.ebu.ch/ publications/funding-of-public-servicemedia>.

- Broadcasting Services Act 1992 (Cth).

- Department of Broadband, Communications and the Digital Economy - Independent Media Inquiry Archived 2012-03-06 at the Wayback Machine

- Stone, Andrew (31 August 2011). "Farewell NZPA, hello three new news services". The New Zealand Herald. Retrieved 31 August 2011.

- Fran O'Sullivan (2016-05-11). "NZME, Fairfax in merger talks". NZ Herald. New Zealand Herald.

- Jdrinnan@Xtra.Co.Nz @Zagzigger2, John Drinnan John Drinnan is the Media Writer for the New Zealand Herald (2011-11-11). "TVNZ and Sky TV too cosy, says industry". The New Zealand Herald. Retrieved 9 January 2016.

- "Sky TV adds to customer base - Business - NZ Herald News". NZ Herald. Nzherald.co.nz. 2001-12-22. Retrieved 2013-04-30.

- Howard, Caroline (December 12, 2016). "Media Concentration In Canada Is Worst In G8: Report". The Huffington Post. Daniel Tencer. Retrieved 2016-12-12.

- Canadian Radio-television and Telecommunications Commission. "About the CRTC". Archived from the original on 20 November 2011. Retrieved 23 October 2011.

- CBCNews (2011-03-11). "Media convergence, acquisitions and sales in Canada". CBC News. Retrieved 24 October 2011.

- Marlow, Iain (2010-09-10). "BCE-CTV deal remakes media landscape". The Globe and Mail. Toronto. Archived from the original on 13 September 2010. Retrieved 2010-09-11.

- McCurry, Lawrence. "Web Exclusive: Media Guilty In G-20". Articles – December 3, 2010. Canadian Dimension. Retrieved 14 January 2012.

- The Globe and Mail (June 22, 2006). "Review media mergers - Senate group urges Grant Robertson and Simon Tuck". The Globe and Mail – republished by Friends of Canadian Broadcasting. Retrieved 10 October 2009.

- Standing Senate Committee on Transport and Communications (June 2006). "Final report on the Canadian news media". Parliament of Canada. Retrieved 10 October 2009.

- "CBC: Feds must examine Irving media empire". 2007-10-12. Retrieved 2016-03-24.

- Venício A. de Lima (2003-07-01). Observatório da Imprensa (ed.). "Existe concentração na mídia brasileira? Sim" (in Portuguese). Retrieved 2012-04-08.

- Castro, D. (2003-03-10). "TV fatura R$ 5,7 bi e cresce 6% em 2002". Folha de S.Paulo (in Portuguese).

- Ortiz, R.; et al. (1989). Brasiliense (ed.). Telenovela-História e Produção. São Paulo.

- Laura Schenkel (2006-09-12). Observatório da Imprensa (ed.). "Formação de monopólio da RBS em SC será questionada" (in Portuguese). Archived from the original on 2013-12-12. Retrieved 2012-04-08.

- Jacques Mick; Lima, Samuel (2006-08-30). Agência Experimental de Jornalismo (ed.). "RBS e AN: os riscos da monopolização" (in Portuguese). Retrieved 2012-04-08.

- Amaral, R.; Guimarães, C. (1994). Journal of Communications (ed.). Media Monopoly in Brazil. 44 (4, Autumm ed.). pp. 30–32.

- Amaral, R.; Guimarães, C. (1994). Journal of Communications (ed.). Media Monopoly in Brazil. 44 (4, Autumm ed.). p. 30.

- Daniel Herz; Görgen, James; Osório, Pedro Luiz (2002-03-06). CartaCapital (ed.). "Quem são os donos" (PDF) (in Portuguese). Archived from the original (PDF) on 2011-11-13. Retrieved 2012-04-05.

- Prof. Murilo César Ramos. University of Brasília (ed.). "Communications regulatory framework in Brazil: media, telecommunications, internet". Archived from the original (pdf) on 2013-10-29. Retrieved 2012-10-16.

- UNESCO (ed.). "Freedom of Expression in Brazil". Retrieved 2012-10-16.

- Maira Magro (2011-01-03). Center for International Media Assistance (ed.). "Brazil's New Communications Minister Defends New Regulation". Archived from the original on 2013-10-29. Retrieved 2012-10-16.

- Rosenfield, Denis (2012-03-27). "Liberdade e regulação". O Estado de S. Paulo (in Portuguese). Archived from the original on 2012-06-01. Retrieved 2013-01-01.

- João Brant (2012-05-17). Carta Maior (ed.). "FHC defende a regulação dos meios de comunicação" (in Portuguese). Archived from the original on 2012-10-22. Retrieved 2012-10-16.

- Mansur, Vinícius (2012-05-22). "Assusta-me que FHC assuma a bandeira da regulação da mídia" (in Portuguese). Carta Maior. Archived from the original on 2013-01-18. Retrieved 2013-01-01.

- ALISON J. HARCOURT (September 1998). "EU Media Ownership Regulation: Conflict over the Definition of Alternatives". Journal of Common Market Studies. 36 (3): 369–389. doi:10.1111/1468-5965.00115.

- Gálik, Mihály (2010). "Regulating Media Concentration within the Council of Europe and the European Union". Media Freedom and Pluralism: Media Policy Challenges in the enlarged Europe [online]. CEUP collection. Budapest: Central European University Press. pp. 229–244. ISBN 9786155211850.

- Pisanò, Alessio (2010) Se il pluralismo scivola in fondo all’agenda Ue, Il Fatto Quotidiano, August 16, 2010

- Alison Harcourt & Robert G. Picard (2009). "Policy, Economic, and Business Challenges of Media Ownership Regulation". Journal of Media Business Studies. 6 (3): 1–17. doi:10.1080/16522354.2009.11073486.

- "European Journalism - Study :Statistical review of journalism and media sector in the European Union". Ec.europa.eu. Retrieved 2013-10-06.

- "Council of Europe". Retrieved 9 January 2016.

- Independent Study on Indicators for Media Pluralism in the Member States – Towards a Risk-Based Approach (PDF). 2009.

- "Monitoring Media Pluralism in Europe: Results of the second pilot-test implementation of the Media Pluralism Monitor (MPM2015)". Archived from the original on 2017-03-23. Retrieved 2017-03-23.

- "MPM 2015 Market Plurality Domain". March 2016. Retrieved 12 March 2017.

- Rtlgroup - About Us

- Media ownership: towards Pan-European groups?. MAVISE.

- Commission of the European Communities, Commission staff working document - Media pluralism in the Member States of the European Union, Brussels, 16.1.2007 SEC(2007) 0032, p.9

- "Independent periodicals", Website of VLTAVA-LABE PRESS a.s. Archived February 6, 2010, at the Wayback Machine: CV Týden, Tachovská Jiskra, Týdeník Domažlicko, Týdeník Chebsko, Týdeník Karlovarska, Týdeník Klatovska, Týdeník Sokolovska, Týdeník Vysočina, Týden u nás, Vyškovské noviny, Nový život, Slovácko, Znojemské noviny, Týdeník Ostrava, Region – Bruntálský, Region – Krnovské noviny, Region – Opavský a Hlučínský, Region – Karvinsko, Region – Havířsko, Region – Týdeník okresu Nový Jičín, Region – Frýdecko-Místecko, Prostějovský týden, Nové Přerovské, Hranický týden, Moravský sever, Slovácké noviny plus

- Company structure on VLTAVA-LABE-PRESS's website Archived February 7, 2010, at the Wayback Machine

- Czech: Website of VLTAVA-LABE PRESS a.s., "About us"

- Czech: Město Brno pohledem lidí z různých oborů BA thesis by Michal Kárný

- "Ročenka Unie vydavatelů 2007". Archived from the original on 17 October 2015. Retrieved 9 January 2016.

- Vltava-Labe-Press AS acquires a minority stake in Prvni Novinova Spolecnost from Czech Republic Thomson Financial Mergers & Acquisitions. 08-06-2001

- Website of VLTAVA-LABE PRESS a.s. Archived 2009-04-30 at the Wayback Machine

- "Verlagsgruppe Passau". Retrieved 9 January 2016.

- The Czech media landscape - print media Archived 2011-03-25 at the Wayback Machine

- Web page of MAFRA

- "Ročenka Unie vydavatelů 2008". Retrieved 9 January 2016.

- "The press in the Czech Republic". BBC News. December 10, 2005. Retrieved 2008-12-13.

- Pre-workshop Report, Robert Schumann centre for Advanced Studies Archived September 29, 2011, at the Wayback Machine

- "Eurozine - The market takes all - Jaromír Volek Czech Republic: Playing the game of media trumps". 2009-03-19. Archived from the original on 5 January 2016. Retrieved 9 January 2016.

- "Rupert Murdoch BSkyB takeover gets government go-ahead". BBC News. 2011-03-03.

- Brook, Stephen; Sweney, Mark (2009-01-21). "Alexander Lebedev's Evening Standard takeover: Dacre announces sale to staff". The Guardian. London. Retrieved 2009-01-21.

- "The Independent bought by Lebedev for £1". BBC News. 2010-03-25. Retrieved 2010-03-25.

- Iyengar, Rishi (2018-07-12). "India now has the 'world's strongest' net neutrality rules". CNNMoney. Retrieved 2020-04-01.

- Verter, Yossi (Feb 10, 2015), Israel election's biggest battle being fought by newspaper tycoons, Haaretz, retrieved October 19, 2015

- Permisos y concesiones de televisión en México Archived 2011-08-24 at the Wayback Machine

- Howard, Caroline (December 12, 2016). "Telecommunications: Mexico's New Reform | Americas Quarterly". americasquarterly.org. Retrieved 2016-12-12.

- Steiner, Tobias. "Under the Macroscope: Convergence in the US Television Market between 2000 and 2014". academia.edu. Retrieved 4 Aug 2015.

- Solomon, Norman (July–August 2005). "The Military-Industrial-Media Complex". Extra!. Fairness and Accuracy in Reporting. Retrieved 2008-12-19.

- Ashley Lutz (14 June 2012). "These 6 Corporations Control 90% Of The Media In America". Business Insider. Retrieved 9 January 2016.

- "AT&T Inc". finance.yahoo.com. Retrieved 2019-11-05.

- "Comcast Corporation". finance.yahoo.com. Retrieved 2019-10-27.

- "The Walt Disney Company". finance.yahoo.com. Retrieved 2019-10-27.

- "CBS Corporation". finance.yahoo.com. Retrieved 2019-10-27.

- "Viacom". finance.yahoo.com. Retrieved 2019-10-27.

- "Fox Corporation". finance.yahoo.com. Retrieved 2019-10-27.

- "News Corp officially splits in two". BBC News. 2013-06-28. Retrieved June 29, 2013.

- Howard, Caroline (2012-10-03). "In depth: Media in Venezuela". BBC News. Retrieved 2016-12-12.

Bibliography

- Doyle, Gillian (2002). Media ownership: the economics and politics of convergence and concentration in the UK and European media. SAGE. ISBN 978-0-7619-6680-7.

- Harcourt, Alison (2005). European Institutions and the Regulation of Media Markets. Manchester University Press. ISBN 978-0-7190-6645-0.

- Harcourt, Alison; Robert Picard (2009). Policy Economic and Business Challenges of Media Ownership Regulation. Journal of Business Media Studies. Archived from the original on 2011-07-23. Retrieved 2011-09-05.

- Steven, Peter (2004). The No-nonsense Guide to Global Media. Verso. ISBN 978-1-85984-581-3.

- Amelia Arsenault & Manuel Castells (2008) The Structure and Dynamics of Global Multi-Media Business Networks. International Journal of Communication.

- Bagdikian, Benjamin H. (2004). The new media monopoly. Beacon Press. ISBN 978-0-8070-6187-9.

- Baker, C. Edwin (2007). Media concentration and democracy: why ownership matters. Cambridge University Press. ISBN 978-0-521-86832-7.

- Compaine, Benjamin M.; Gomery, Douglas (2000). Who owns the media?: competition and concentration in the mass media industry. Psychology Press. ISBN 978-0-8058-2936-5.

- Croteau, David; Hoynes, William (2006). The business of media: corporate media and the public interest. Pine Forge Press. ISBN 978-1-4129-1315-7.

- Dwyer, Tim (2010). Media Convergence. McGraw-Hill International. ISBN 978-0-335-22873-7.

- Harper, Joe; Yantek, Thom, eds. (2003). Media, profit, and politics: competing priorities in an open society. Kent State University Press. ISBN 978-0-87338-754-5.

- Hassan, Robert; Thomas, Julian, eds. (2006). The new media theory reader. McGraw-Hill International. ISBN 978-0-335-21710-6.

- McChesney, Robert W. (1997). Corporate Media and the Threat to Democracy. Seven Stories Press. ISBN 978-1-888363-47-0.

- Noam, Eli M. (2009). Media ownership and concentration in America. Oxford University Press. ISBN 978-0-19-518852-3.

- Skinner, David; et al., eds. (2005). Converging media, diverging politics: a political economy of news media in the United States and Canada. Lexington Books. ISBN 978-0-7391-1306-6.

- Media convergence. The Canadian Encyclopedia. Retrieved 2011-05-02.

Film

- Manufacturing Consent: Noam Chomsky and the Media (1992)

- Orwell Rolls in His Grave (2004) documentary available on DVD considers media concentration in the U.S.

- Beyond Citizen Kane by Simon Hartog (1993); about Roberto Marinho's Globo Group in Brazil

- Broadcast Blues (2009) Award-winning documentary by former Emmy Winning Radio and TV producer Sue Wilson available on DVD <http://www.SueWilsonReports.com> shows how poor U.S. media policy created media consolidation and teaches people how to force broadcasters to serve the public interest.

External links

- Global Issues.com

- Who Owns What by the Columbia Journalism Review

- Structure and Dynamics of the Global Multi-Media Business Networks Amelia Arsenault and Manuel Castells (2008) International Journal of Communication

- Who Owns What on Television

- Essay examining the reasons and consequences of media ownership

- Campaign For Democratic Media Canadian organization fighting for democratic media.

- Free Press an organization opposing media ownership concentration

- A visual representation of 25 years of media mergers and how the biggest media conglomerates in the United States came to be

- Lasar's Letter on the Federal Communications Commission Media ownership controversy timeline, 1996–2004

- Media ownership study ordered destroyed

- Media Conglomerates, Mergers, Concentration of Ownership

- Media Ownership Chart by watchdog group MediaChannel

- Why TV sucks A critique of the concentration thesis from the left

- FCC Hearing on Media Consolidation, Seattle, Nov 2007 Video of public testimony

- Treepex - Online Newspaper subcategory Increased concentration of media ownership has adverse effects on the pluralism of media output.

- The Campaign for Press and Broadcasting Freedom (CPBF) – a UK-based organisation campaigning for open, accountable and democratic media

- The Day That TV News Died – Pulitzer Prize–winning journalist Chris Hedges on corporate media control.

Supporting Media Deregulation:

Opposing Media Deregulation: