Prospect theory

Prospect theory is a theory in cognitive psychology that describes the way people choose between probabilistic alternatives that involve risk, where the probabilities of outcomes are uncertain. The theory states that people make decisions based on the potential value of losses and gains rather than the final outcome, and that people evaluate these losses and gains using some heuristics. The model is descriptive: it tries to model real-life choices, rather than optimal decisions, as normative models do.

The theory was created in 1979 and developed in 1992 by Daniel Kahneman and Amos Tversky as a psychologically more accurate description of decision making, compared to the expected utility theory. In the original formulation, the term prospect referred to a lottery. The paper "Prospect Theory: An Analysis of Decision under Risk" (1979) has been called a "seminal paper in behavioral economics".[1]

Model

The theory describes the decision processes in two stages:[2]

- During an initial phase termed editing, outcomes of a decision are ordered according to a certain heuristic. In particular, people decide which outcomes they consider equivalent, set a reference point and then consider lesser outcomes as losses and greater ones as gains. The editing phase aims to alleviate any framing effects.[3] It also aims to resolve isolation effects stemming from individuals' propensity to often isolate consecutive probabilities instead of treating them together. The editing process can be viewed as composed of coding, combination, segregation, cancellation, simplification and detection of dominance.

- In the subsequent evaluation phase, people behave as if they would compute a value (utility), based on the potential outcomes and their respective probabilities, and then choose the alternative having a higher utility.

The formula that Kahneman and Tversky assume for the evaluation phase is (in its simplest form) given by:

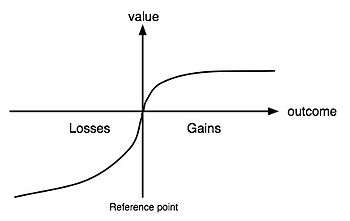

where is the overall or expected utility of the outcomes to the individual making the decision, are the potential outcomes and their respective probabilities and is a function that assigns a value to an outcome. The value function that passes through the reference point is s-shaped and asymmetrical. Losses hurt more than gains feel good (loss aversion). This differs from expected utility theory, in which a rational agent is indifferent to the reference point. In expected utility theory, the individual does not care how the outcome of losses and gains are framed. The function is a probability weighting function and captures the idea that people tend to overreact to small probability events, but underreact to large probabilities. Let denote a prospect with outcome with probability and outcome with probability and nothing with probability . If is a regular prospect (i.e., either , or , or ), then:

However if and either or , then:

![V(x,p;y,q)=\nu(y)+\pi(p) \left[ \nu (x)- \nu (y) \right]](../I/m/b5cec2d80caa277c631bcd526d35ecb2d65e4469.svg)

It can be deduced from the first equation that and . The value function is thus defined on deviations from the reference point, generally concave for gains and commonly convex for losses and steeper for losses than for gains. If is equivalent to then is not preferred to , but from the first equation it follows that , which leads to , therefore:

This means that for a fixed ratio of probabilities the decision weights are closer to unity when probabilities are low than when they are high. In prospect theory, is never linear. In the case that , and prospect dominates prospect , which means that , therefore:

As , , but since , it would imply that must be linear, however dominated alternatives are brought to the evaluation phase since they are eliminated in the editing phase. Although direct violations of dominance never happen in prospect theory, it is possible that a prospect A dominates B, B dominates C but C dominates A.

Example

To see how prospect theory can be applied, consider the decision to buy insurance. Assume the probability of the insured risk is 1%, the potential loss is $1,000 and the premium is $15. If we apply prospect theory, we first need to set a reference point. This could be the current wealth or the worst case (losing $1,000). If we set the frame to the current wealth, the decision would be to either

1. Pay $15 for sure, which yields a prospect-utility of ,

OR

2. Enter a lottery with possible outcomes of $0 (probability 99%) or −$1,000 (probability 1%), which yields a prospect-utility of .

According to prospect theory,

- , because low probabilities are usually overweighted;

- , by the convexity of value function in losses.

The comparison between and is not immediately evident. However, for typical value and weighting functions, , and hence . That is, a strong overweighting of small probabilities is likely to undo the effect of the convexity of in losses, making the insurance attractive.

If we set the frame to -$1,000, we have a choice between and . In this case, the concavity of the value function in gains and the underweighting of high probabilities can also lead to a preference for buying the insurance.

The interplay of overweighting of small probabilities and concavity-convexity of the value function leads to the so-called fourfold pattern of risk attitudes: risk-averse behavior when gains have moderate probabilities or losses have small probabilities; risk-seeking behavior when losses have moderate probabilities or gains have small probabilities.

Below is an example of the fourfold pattern of risk attitudes. The first item in each quadrant shows an example prospect (e.g. 95% chance to win $10,000 is high probability and a gain). The second item in the quadrant shows the focal emotion that the prospect is likely to evoke. The third item indicates how most people would behave given each of the prospects (either Risk Averse or Risk Seeking). The fourth item states expected attitudes of a potential defendant and plaintiff in discussions of settling a civil suit.[4]

| Example | Gains | Losses |

|---|---|---|

| High probability (certainty effect) | 95% chance to win $10,000 or 100% chance to obtain $9,499. So, 95% × $10,000 = $9,500 > $9,499. Fear of disappointment. Risk averse. Accept unfavorable settlement of 100% chance to obtain $9,499 | 95% chance to lose $10,000 or 100% chance to lose $9,499. So, 95% × −$10,000 = −$9,500 < −$9,499. Hope to avoid loss. Risk seeking. Rejects favorable settlement, chooses 95% chance to lose $10,000 |

| Low probability (possibility effect) | 5% chance to win $10,000 or 100% chance to obtain $501. So, 5% × $10,000 = $500 < $501. Hope of large gain. Risk seeking. Rejects favorable settlement, chooses 5% chance to win $10,000 | 5% chance to lose $10,000 or 100% chance to lose $501. So, 5% × −$10,000 = −$500 > −$501. Fear of large loss. Risk averse. Accept unfavorable settlement of 100% chance to lose $501 |

Probability distortion is that people generally do not look at the value of probability uniformly between 0 and 1. Lower probability is said to be over-weighted (that is a person is over concerned with the outcome of the probability) while medium to high probability is under-weighted (that is a person is not concerned enough with the outcome of the probability). The exact point in which probability goes from over-weighted to under-weighted is arbitrary, however a good point to consider is probability = 0.33. A person values probability = 0.01 much more than the value of probability = 0 (probability = 0.01 is said to be over-weighted). However, a person has about the same value for probability = 0.4 and probability = 0.5. Also, the value of probability = 0.99 is much less than the value of probability = 1, a sure thing (probability = 0.99 is under-weighted). A little more in depth when looking at probability distortion is that π(p) + π(1 − p) < 1 (where π(p) is probability in prospect theory).[5]

Applications

Some behaviors observed in economics, like the disposition effect or the reversing of risk aversion/risk seeking in case of gains or losses (termed the reflection effect), can also be explained by referring to the prospect theory.

The pseudocertainty effect is the observation that people may be risk-averse or risk-acceptant depending on the amounts involved and on whether the gamble relates to becoming better off or worse off. This is a possible explanation for why the same person may buy both an insurance policy and a lottery ticket.

An important implication of prospect theory is that the way economic agents subjectively frame an outcome or transaction in their mind affects the utility they expect or receive. Narrow framing is a derivative result which has been documented in experimental settings by Tversky and Kahneman,[6] whereby people evaluate new gambles in isolation, ignoring other relevant risks. This phenomenon can be seen in practice in the reaction of people to stock market fluctuations in comparison with other aspects of their overall wealth; people are more sensitive to spikes in the stock market as opposed to their labor income or the housing market.[7] It has also been shown that narrow framing causes loss aversion among stock market investors.[8] This aspect has also been widely used in behavioral economics and mental accounting.

The digital age has brought the implementation of prospect theory in software. Framing and prospect theory has been applied to a diverse range of situations which appear inconsistent with standard economic rationality: the equity premium puzzle, the excess returns puzzle and long swings/PPP puzzle of exchange rates through the endogenous prospect theory of Imperfect Knowledge Economics, the status quo bias, various gambling and betting puzzles, intertemporal consumption, and the endowment effect. It has also been argued that prospect theory can explain several empirical regularities observed in the context of auctions (such as secret reserve prices) which are difficult to reconcile with standard economic theory.[9]

Limits and extensions

The original version of prospect theory gave rise to violations of first-order stochastic dominance. That is, prospect A might be preferred to prospect B even if the probability of receiving a value x or greater is at least as high under prospect B as it is under prospect A for all values of x, and is greater for some value of x. Later theoretical improvements overcame this problem, but at the cost of introducing intransitivity in preferences. A revised version, called cumulative prospect theory overcame this problem by using a probability weighting function derived from rank-dependent expected utility theory. Cumulative prospect theory can also be used for infinitely many or even continuous outcomes (for example, if the outcome can be any real number).

Critics from the field of psychology argued that even if Prospect Theory arose as a descriptive model, it offers no psychological explanations for the processes stated in it[10]. Furthermore, factors that are equally important to decision making processes have not been included in the model, such as emotion.[11]

See also

Notes

- ↑ Shafir & LeBoeuf 2002.

- ↑

- Kahneman, Daniel; Tversky, Amos (1979). "Prospect Theory: An Analysis of Decision under Risk" (PDF). Econometrica. 47 (2): 263. doi:10.2307/1914185. ISSN 0012-9682.

- ↑ Tversky & Kahneman 1986.

- ↑ Kahneman 2011, p. 317.

- ↑ Baron 2006, pp. 264–266.

- ↑ Tversky, Amos; Kahneman, Daniel (1986). "Rational Choice and the Framing of Decisions*". The Journal of Business. 59 (4): 251–278. doi:10.1007/978-3-642-74919-3_4.

- ↑ Barberis, Nicholas; Heung, Ming; Thaler, Richard H. (2006). "Individual preferences, monetary gambles, and stock market participation: a case for narrow framing". American Economic Review. 96 (4): 1069–1090. doi:10.1257/aer.96.4.1069.

- ↑ Benartzi, Shlomo; Thaler, Richard (1995). "Myopic loss aversion and the Equity Premium Puzzle". The Quarterly Journal of Economics. 110 (1): 453–458. doi:10.2307/2118511.

- ↑ Rosenkranz, Stephanie; Schmitz, Patrick W. (2007). "Reserve Prices in Auctions as Reference Points". The Economic Journal. 117 (520): 637–653. doi:10.1111/j.1468-0297.2007.02044.x. ISSN 1468-0297.

- ↑ Staddon, John (2017) Scientific Method: How science works, fails to work or pretends to work. Taylor and Francis.

- ↑ Newell, Benjamin, R.; Lagnado, David, A.; Shanks, David, R. (2007). Straight choices: The psychology of decision making. New York: Psychology Press. ISBN 978-1841695891.

Further reading

- Easterlin, Richard A. "Does Economic Growth Improve the Human Lot?", in Abramovitz, Moses; David, Paul A.; Reder, Melvin Warren (1974). Nations and Households in Economic Growth: Essays in Honor of Moses Abramovitz. Academic Press. ISBN 978-0-12-205050-3. Retrieved 2016-03-10.

- Frank, Robert H. (1997). "The frame of reference as a public good". The Economic Journal. 107 (445): 1832–1847. doi:10.1111/j.1468-0297.1997.tb00086.x. ISSN 0013-0133.

- Kahneman, Daniel (2011). Thinking, Fast and Slow. Farrar, Straus and Giroux. ISBN 978-1-4299-6935-2. Retrieved 2016-03-10.

- Kahneman, Daniel; Tversky, Amos (1979). "Prospect Theory: An Analysis of Decision under Risk" (PDF). Econometrica. 47 (2): 263. doi:10.2307/1914185. ISSN 0012-9682.

- Tversky, Amos; Kahneman, Daniel (1992). "Advances in prospect theory: Cumulative representation of uncertainty". Journal of Risk and Uncertainty. 5 (4): 297–323. doi:10.1007/BF00122574. ISSN 0895-5646.

- Lynn, John A. (1999). The Wars of Louis XIV 1667-1714. Routledge. ISBN 9780582056299. Retrieved 2016-03-10.

- McDermott, Rose; Fowler, James H.; Smirnov, Oleg (2008). "On the Evolutionary Origin of Prospect Theory Preferences". The Journal of Politics. 70 (02). doi:10.1017/S0022381608080341. ISSN 0022-3816.

- Post, Thierry; van den Assem, Martijn J; Baltussen, Guido; Thaler, Richard H (2008). "Deal or No Deal? Decision Making under Risk in a Large-Payoff Game Show". American Economic Review. 98 (1): 38–71. doi:10.1257/aer.98.1.38. ISSN 0002-8282.

- Baron, Jonathan (2006). Thinking and Deciding (4th ed.). Cambridge University Press. ISBN 978-1-139-46602-8. Retrieved 2016-03-10.

- Tversky, Amos; Kahneman, Daniel (1986). "Rational Choice and the Framing of Decisions" (PDF). The Journal of Business. 59 (S4): S251. doi:10.1086/296365.

- Shafir, Eldar; LeBoeuf, Robyn A. (2002). "Rationality". Annual Review of Psychology. 53 (1): 491–517. doi:10.1146/annurev.psych.53.100901.135213. ISSN 0066-4308. PMID 11752494.

- Dacey, Raymond; Zielonka, Piotr (2013). "High volatility eliminates the disposition effect in a market crisis". Decyzje. doi:10.7206/DEC.1733-0092.9.